Equity

Key takeaways

- Q3 company earnings offered a lot to cheer, though market action implies a greater mix of emotions as positive earnings compete with AI skepticism.

- Equity CIO Carrie King believes the AI influence is enduring and sees growing opportunity for stock selection as winners and losers emerge.

- She suggests bubble worries may be overblown and notes that stock prices move much faster and more frequently than company fundamentals.

This article has additional related content

U.S. stocks, as measured by the S&P 500 Index, are on pace for 14% growth in earnings for Q3 2025. This marks the fourth consecutive quarter of double-digit growth and comes in well ahead of analysts’ Sept. 30 estimates of 7%.

The “Magnificent 7” stocks were standouts once again, growing earnings per share (EPS) 21% in the quarter compared to 13% for the “other 493.” Our data shows 85% of companies beating their EPS estimates, though market reaction showed a smaller price reward for beats and greater punishment for misses than historically has been the case. This is likely a reflection of the market’s high expectations after what’s shaping up to be a third consecutive year of healthy gains.

Against this backdrop ― and amid recent whiffs of AI consternation ― we offer three reflections anchored in the most recent quarter’s earnings:

Even “wow” comes in degrees

Within the context of an exceptional quarter at the index level, there were clearly leaders and laggards. Even in those sectors that wowed, we saw notable differentiation.

Of the four S&P 500 sectors that have driven performance year-to-date (utilities, communication services, IT and industrials), all but one notched Q3 earnings growth above the Mag 7. Communication services was the exception, weighed down by disappointing results from a Mag 7 constituent.

The upshot: Even the top tier features differentiation. Dispersion crosses sectors, themes and the individual stocks within them, and this means exciting potential to generate alpha through skilled stock selection.

The top-earning sector this quarter was IT, boasting 40% EPS growth. Over 90% of companies beat revenue estimates and almost all (98%) exceeded EPS growth estimates. Yet from a return perspective, our analysis as of Nov. 14, 2025, found a 305% difference between IT’s top and bottom performers.

AI the defining line

Each of the S&P’s top-performing sectors of the year has a distinct AI influence. Likewise, AI was the defining line between leaders and laggards within these sectors.

In IT, we observe the picks and shovels of the AI buildout disrupting traditional software and services. In utilities, we see a preference for areas likely to grow amid AI data center energy needs, including nuclear, renewables and gas. And in industrials, we find that companies enabling the AI revolution are preferred over cyclically exposed transportation companies. Power providers and manufacturers of cooling systems and components reported large jumps in orders in the quarter on AI data center demand.

This type of nuance and dispersion speaks to the importance of deep bottom-up analysis to fully understand the business case and fundamental strength of each company considered for investment.

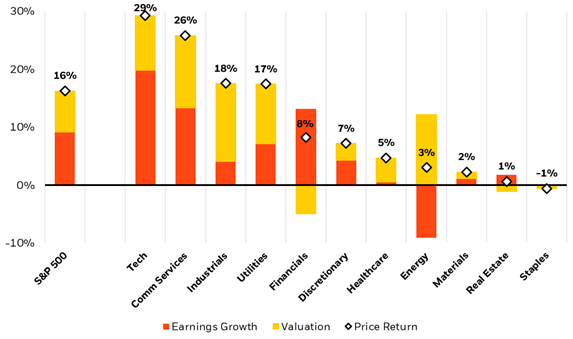

While recent talk of a market bubble has caused a pullback in the AI trade and the stocks of key beneficiaries, we remain optimistic. Ai is a multi-year investment theme poised to create new business models across industries, and its strong performance is not based on hope but on fundamentals. As shown in the chart below, the return of tech and some other AI-exposed sectors has been driven more by earnings than multiple expansion. Our analysis found the earnings contribution to be even greater among the AI-powered tech leaders. As AI progress advances and more use cases emerge, we expect it to continue to drive differentiation throughout the market as some business models thrive while others are disrupted.

AI outperformance backed by fundamentals

Return composition of S&P 500 sectors, 2025 to date

Source: BlackRock Fundamental Equities with data from FactSet, Oct. 31, 2025. Past performance is not indicative of current or future results. Indexes are unmanaged and it is not possible to invest directly in an index.

Opportunity beyond AI

Our optimism isn’t only about AI. Other standouts in the third quarter earnings season included financials (23% EPS growth and 90% of companies beating EPS forecasts), where ytd returns also have been driven by earnings (see chart above). We see further tailwinds supporting the banks, including potential for deregulation that already seems to be boosting M&A activity, and a generally healthy credit outlook, with stability in loan books and delinquency rates.

In industrials, though AI-adjacent companies retain the upper hand, we saw improving orders among cyclically exposed segments and above-consensus earnings growth that could be signaling better times ahead. The sector has performed well this year (see chart) as valuations appear to be pricing in good news to come.

The story was different for consumer companies, which collectively had a difficult earnings season. We still see bifurcation between the stressed lower-income consumer and mid- to higher-income counterparts, and a value-seeking mindset overall. While “tariff” mentions on earnings calls fell this quarter, according to data from FactSet, 79% of consumer staples calls still made mention, the highest of all sectors. Pre-ordering of inventory may have softened some tariff impact to date, as company margins have held up well, but we are watchful for any change here and look to the holiday shopping season for more clues on consumer health.

Year-end market reflections

U.S. stocks endured a series of worries in 2025, starting with DeepSeek-related AI fears in late January, the “tariff tantrum” in early April, intermittent macro-induced ebbs and flows, and more recent concern of an AI bubble. Yet through each quarter, company earnings growth held steady or improved. We offer two broad reflections as we kick off the season of good cheer:

- Stock prices move much faster and more frequently than company fundamentals. Having a solid understanding of those fundamentals can offer some solace amid inevitable bouts of volatility.

- Corporate America demonstrates a unique dynamism that we believe provides the resourcefulness and elasticity to weather changing markets. But of course, it also represents a fantastically heterogeneous group of opportunities that we believe is best navigated with a fundamental active approach to investment.

Carrie King

CIO of U.S. and Developed Markets, BlackRock Fundamental Equities

Investments

Insights

Retirement

Tools

Resources

About Us

Earnings figures cited herein are from BlackRock Fundamental Equities, with data from Refinitiv and FactSet as of Nov. 19, 2025, with 452 companies (82% of S&P 500 market cap) reporting. Year-over-year figures compare currently reported data to full-quarter data one year prior and are subject to change.

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of November 2025 and may change as subsequent conditions vary. The information and opinions contained in this post are derived from proprietary and nonproprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This post may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this post is at the sole discretion of the reader. Past performance is no guarantee of future results.

Investing involves risk. Equities may decline in value due to both real and perceived general market, economic, and industry conditions. Diversification does not ensure profits or protect against loss.

AI technology relies on large data sets, which can lead to inaccuracies. Companies in AI face competition, rapid obsolescence, and depend on demand from various industries. Regulatory scrutiny could limit AI development, with data collection facing closer examination and potential fines. Country-specific regulations could also impact AI and big data companies.

The Funds are actively managed and do not seek to replicate the performance of a specified index, may have higher portfolio turnover, and may charge higher fees than index funds due to increased trading and research expenses.

Active funds are subject to management risk, which means the fund manager's techniques may not produce desired results, and the selected securities may not align with the fund's investment objective. Legislative, regulatory, or tax developments may also affect the fund manager's ability to achieve the investment objective.

Carefully consider the Funds' investment objectives, risk factors, and charges and expenses before investing. This and other information can be found in the Funds' prospectuses or, if available, the summary prospectuses, which may be obtained by visiting the BlackRock Fund prospectus pages. Read the prospectus carefully before investing.

Prepared by BlackRock Investments, LLC, member FINRA.

©2026 BlackRock, Inc. or its affiliates. All Rights Reserved. BLACKROCK and iSHARES are trademarks of BlackRock, Inc. or its affiliates. All other trademarks are those of their respective owners.

USRRMH1125U/S-5019318