Precious metals are having a moment. Gold and silver surged to record highs in January, benefiting from an alignment of macroeconomic factors, evolving supply-demand dynamics, and renewed industrial demand. But they are also entering a more volatile phase. After the announcement of Kevin Warsh as the nominee for Federal Reserve Chair prompted a rally in the dollar, both metals saw their largest single-day declines in more than three decades. While some of the dip was likely attributed to technical factors like large derivatives usage and low liquidity into month end, the speed of the sell-off surprised many allocators.

After a record run – and a sharp decline – where do precious metals go from here? And how do they fit into investor portfolios? We break it down below.

What is happening with gold and silver prices right now?

- Gold: The price of gold has soared 75% in the past year, surpassing $5,000/oz for the first time in January, before tumbling 12% on month end.1 The rush for gold comes from a variety of buyers, ranging from central banks to cryptocurrencies.2

- Silver: Silver rose by 148% in 2025, adding another 19% in January – even after accounting for the 26% decline on Jan 30th.3 The surge has reflected strong investor and industrial demand as well as a less liquid market.

- Volatility in gold and silver has jumped 46% and 106% year-to-date respectively, reinforcing that this rally is powerful, but not without risk.4

What’s causing the moves in gold and silver?

There are three key drivers of recent performance:

1. Mounting government debts has made metals attractive as a store of value.

Government debt levels have risen to concerning levels globally. In the U.S., federal debt now exceeds 120% of GDP, while annual fiscal deficits continue to run near 6–7% of GDP. And it’s not alone: global debt has surpassed 100% of GDP for major developed economies like Japan, the U.K., France and Canada as well.5

Although also associated with other risks, gold’s role as a potential store of value with no sovereign issuer risk has historically resonated in such environments.6 Silver has often behaved as a higher-beta extension of this theme, though its pricing reflects a combination of investment flows and industrial demand. Over the past 20 years, silver’s annualized volatility has been up to twice that of gold, underscoring its more cyclical nature.7

2. Political and geopolitical uncertainty spurs safe-haven demand.

Periods of policy transition and global re-alignment often increase demand for perceived safe haven assets. But rather than view precious metals purely as a haven, we believe they are best understood as portfolio stabilizers that have historically shown low or negative correlation to equities during periods of market stress.

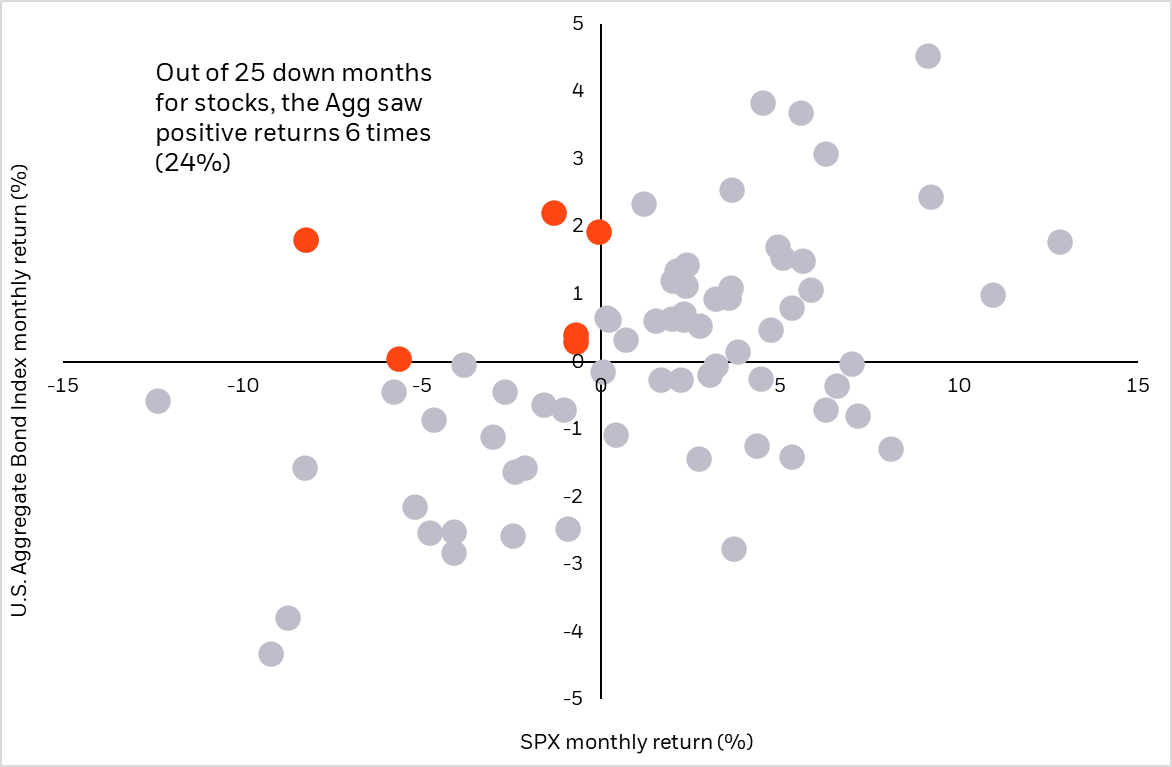

Diversification matters most when equities are falling. Since 2020, during months when the S&P 500 declined more than 5%, gold has delivered an average return of 2%, while the U.S. Aggregate Bond Index has been closer to flat.8 This asymmetry makes gold particularly valuable in drawdown scenarios.

Figure 1: Out of 25 down months for stocks, gold saw positive returns 40% of the time