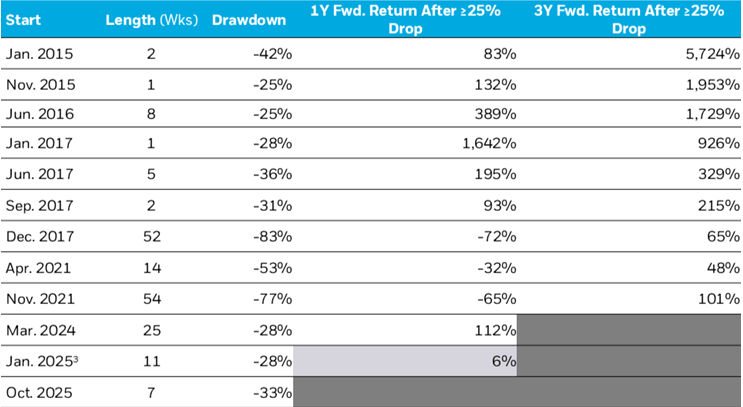

Over the past few weeks, bitcoin and the longer tail of crypto assets have experienced a sharp pullback, materially outpacing more modest corrections seen in broader markets.

After reaching its all-time high of $126K in early October, bitcoin fell as low as $84k or ~33%.1 The recent price action cannot be attributed to a single headline event or catalyst. Instead, in our view, it reflects a confluence of loosely connected factors and evolving market structure dynamics:

Shift in Fed Outlook: Expectations for slower Fed rate cuts have pushed real yields higher. For context, in October the market was pricing in a ~30% chance of one rate cut or fewer. As of early December, markets are pricing about a 46% chance of one rate cut or fewer by the March 2026 Fed meeting.2 While bitcoin’s fundamentals are largely detached from traditional economic drivers or country-specific risks, bitcoin has historically shown sensitivity to USD real rates, similar to gold and emerging-market currencies. The latest dip, on Nov. 30, occurred during a low-liquidity holiday weekend evening in the U.S.

Unwind of Excessive Leverage: Heavy use of leveraged perpetual futures in cryptoasset trading amplified short-term speculation and appears to have precipitated a “flash crash” on Oct. 10, when an initial price drop triggered automated forced liquidation of long positions, adding substantial selling pressure and setting off a chain effect that ultimately erased over 30% of futures open interest3. Lingering aftereffects of this leverage-driven sell-off persist, contributing to an overhang in the market.

Whales Rebalancing: For a substantial cohort of long-time bitcoin holders (many with cost bases of <$1k, “Whales”), $100K represented a key psychological milestone and implicit portfolio rebalancing trigger. We observe that crossing this threshold prompted some investors with concentrated exposure begin reducing overly concentrated bitcoin positions, thereby adding incremental selling pressure to the market.

Unwind of Digital Asset Treasury Optimism: Shares of digital asset treasury companies (DATs) have sold off sharply QTD and now predominantly trade near or below the NAV of the bitcoin holdings. The large premiums that spurred a flurry of new listings earlier this year have vanished, removing a source of buying pressure and raising questions of whether some treasury companies will conduct asset sales to bring their share prices back to NAV.