Sustainable Investing1

Sustainable investing is used as an umbrella term to describe investment strategies that combine traditional security analysis with environmental, social, and governance insights.

ESG describes the Environmental (E), Social (S), and Governance (G) metrics that are evaluated to inform security selection.

![Image describing ESG definitions.]()

ESG analysis evaluates risks and opportunities beyond the scope of traditional financial analysis.

![ESG risks and opportunities breakdown.]()

Overview of MSCI ESG Fund Ratings1

MSCI rated companies according to their exposure to industry-specific ESG risks, and opportunities and their ability to manage those risks and opportunities relative to peers.

The company level ratings are aggregated to the fund level by MSCI, which are further aggregated to the portfolio level by BlackRock using MSCI-provided calculations to display the portfolio-level ESG rating in the 360 Evaluator.

The key issue scores and weights are combined and normalized per industry to offer an overall MSCI ESG score (0-10) and MSCI ESG Rating (AAA-CCC) for each issuer.

![MSCI ESG rating process and score range.]()

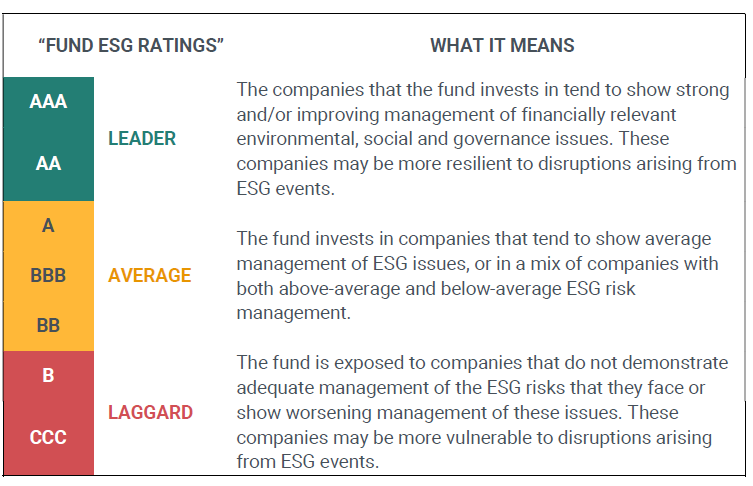

MSCI ESG Fund Ratings and MSCI ESG Fund Quality Scores2

The MSCI ESG Fund Rating is designed to assess the resilience of a fund’s aggregate holdings to long-term, financially relevant, ESG risks. MSCI ESG Fund Ratings aim to help investors better understand the ESG characteristics of a fund. The MSCI ESG Fund Rating is based on the MSCI ESG Fund Quality Score.

The MSCI ESG Fund Quality Score is provided on a 0-10 scale, with 0 and 10 being the respective lowest and highest possible fund scores. The MSCI ESG Fund Rating is provided on a AAA-CCC scale, with AAA and CCC being the highest and lowest possible fund ratings, respectively.

![The MSCI ESG Fund Quality Score rating chart and what it means.]()

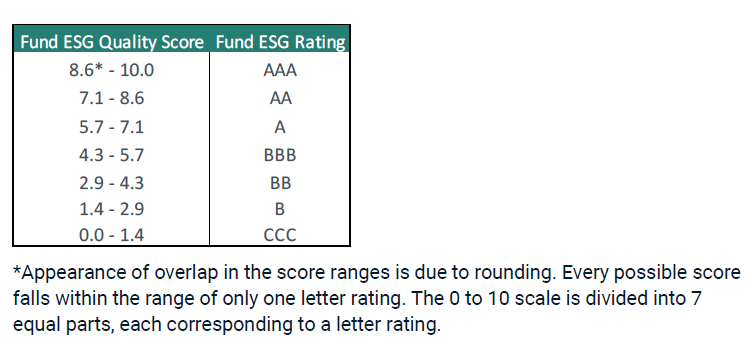

Derivation of MSCI ESG Fund Rating from underlying company scores2

The MSCI ESG Fund Quality Score and the MSCI ESG Fund Rating are derived from the asset-weighted average of MSCI ESG Ratings of a fund’s underlying holdings.

The MSCI ESG Fund Quality Score is a 0-10 score calculated based on the weighted average ESG score of the underlying holdings, rescaled to account for ESG coverage.

The MSCI ESG Fund Rating is a direct mapping to the 0-10 MSCI ESG Fund Quality Score per table below. The 0 to 10 scale is divided into seven equal parts, each corresponding to a Fund ESG Rating letter rating. Every possible MSCI ESG Fund Quality Score falls within the range of only one letter rating.

![Table showing derivation of MSCI ESG Fund Rating from underlying company scores.]()

Funds included in MSCI ESG Fund Ratings2

To be included in MSCI ESG Fund Ratings, a fund must pass the following three criteria:

- 60% of the fund’s gross weight (or 45% for bond funds and money market funds) must come from securities with ESG coverage by MSCI ESG Research (certain cash positions and other asset types like securitized products, commodities, currency, and others are not currently covered by ESG analysis by MSCI are removed prior to calculating a fund’s gross weight; the absolute values of short positions are included but treated as uncovered)

- Updated Holdings Data: Fund holdings date must be less than one year old.

- Portfolio Holdings Minimum: Fund must have at least ten securities.

Calculation of portfolio level ESG metrics

The portfolio ESG Rating and Environmental, Social, and Governance Scores are computed by BlackRock, using the formulas provided by MSCI, and based on the weighted average ESG Scores of the underlying funds & stocks within the portfolio.

- ESG Ratings Methodology, April 2024 - https://www.msci.com/documents/1296102/34424357/MSCI+ESG+Ratings+Methodology.pdf.

- MSCI ESG Fund Ratings Methodology, March 2025 - https://www.msci.com/documents/1296102/34424357/MSCI+ESG+Fund+Ratings+Methodology.pdf.