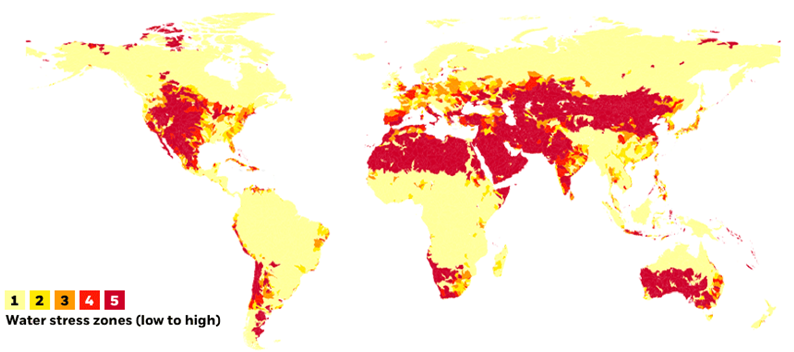

We use the U.S. Southwest to illustrate our methodology. We use 2014 (actual) as our baseline because WRI’s data draw on an extensive modeling and simulation project ran by Utrecht University that spanned 1960-2014. This data represents the most recent and accurate global picture of water stress available, we believe.

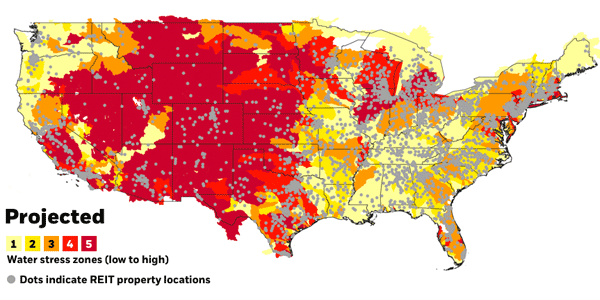

Key assumptions: Almost the entire U.S. Southwest, including states such as California, Arizona, New Mexico and Utah, faces extreme water stress issues by 2030. Most of the current REIT properties in the region, indicated by the grey dots, lie in these high risk zones.

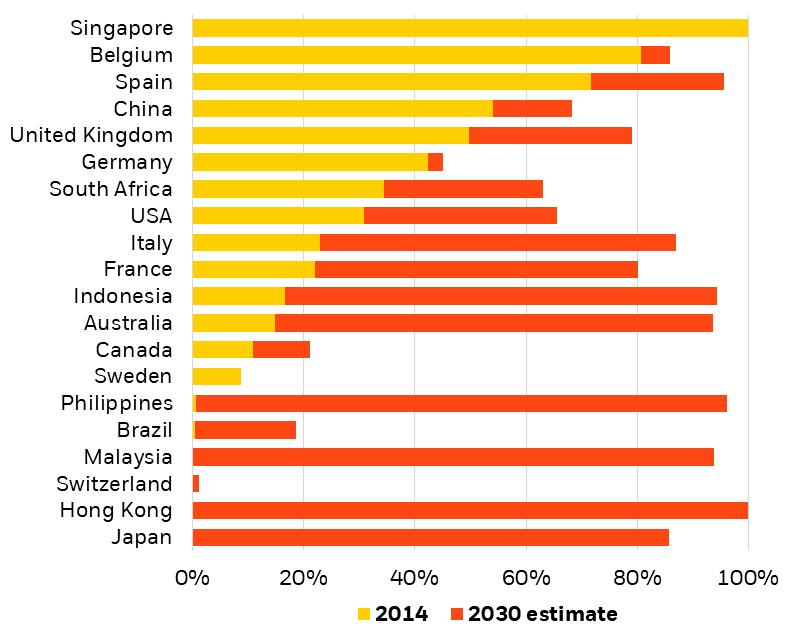

Roughly 60% of the global REIT properties we were able to geolocate will experience high water stress by 2030, we find, driven by increased urbanization and the effects of climate change. This is more than double the number today. Water-related issues are not yet a material cash-flow driver for REITs, in our view, and the risks can be mitigated. Yet they may become more material over time due to knock-on effects such as regulatory shifts.

Almost all REIT properties in Malaysia, Philippines, Japan, Hong Kong and Australia will likely be in high risk water zones by 2030, our analysis shows. Roughly two-thirds of today’s U.S. REIT properties will be at high risk of water stress by 2030, double the proportion today, we also conclude.

Investors and tenants are increasingly focused on water stress, as well as other environmental factors such as energy efficiency, green certifications and carbon footprints. REITs that score highly on these metrics can potentially save costs, while screening as more “green.” This may make their equities more attractive to potential investors and their buildings more desirable for occupants.

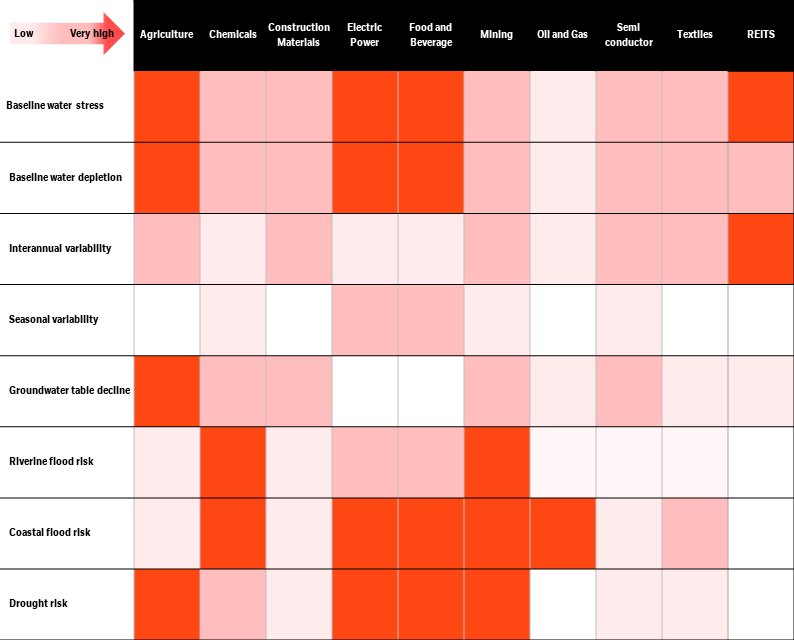

Water stress has wide-ranging implications across asset classes. We show how the agriculture, electric power and food and beverage industries may be most at risk. The creditworthiness of some countries, states and municipalities facing shortages could also come under threat as they face additional costs to fortify their water infrastructure. This comes on top of other growing physical climate risks such as exposure to flooding and other extreme weather events.

Companies resilient to water stress and other climate-related risks may fetch a premium in the transition to a more sustainable world, we believe. Better understanding and quantifying the risks can help investors mitigate exposures and potentially exploit any mispricing. Related data and insights are valuable tools for investors to engage with companies and issuers on their sustainability-related efforts.