More resources

Debunking 3 investor myths on volatility

Learn how to avoid some common pitfalls when it comes to saving for retirement in a volatile market.

To reach a different BlackRock site directly, please update your user type.

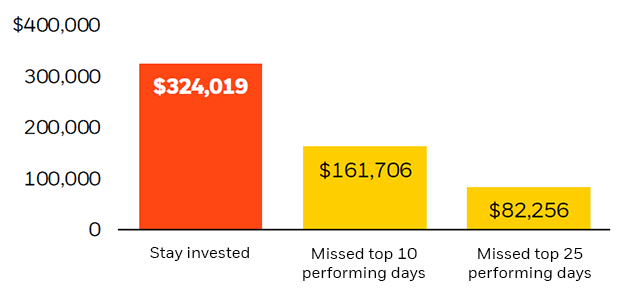

Staying invested can increase the possibility of greater earning, sometimes more than double that of a portfolio which misses top performing market days.

Every major market decline from 1987 through 2022 in U.S. equities has reversed itself, sometimes as much as 68%, within the following year.1 This type of market trend reinforces the importance of focusing on the future as opposed to short-term disruptions.

For those thinking about withdrawing from retirement savings, consider: your plan’s rules, other sources of emergency funds, potential financial implications, seeking out professional advice and that unrepaid loans may be treated like income.

Historically, stock market downturns are often followed by a period of positive market performance.

Source: Morningstar. Returns are principal only not including dividends. Stocks are represented by the S&P 500 Index, an unmanaged index that is generally considered representative of the U.S. stock market. Past performance is no guarantee of future results. For illustrative purposes only. It is not possible to invest directly in an index.

Every major decline from 1987 through 2022 in U.S. equities has reversed itself between 21% and 68% within the following year.

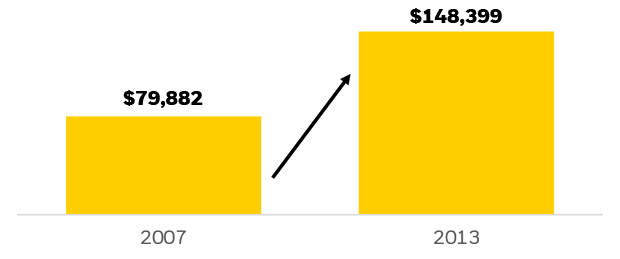

Investors who can continue contributing to their retirement have the potential to take advantage of market recoveries. For example, those who stayed in their plan from 2007 through 2013 saw their average account balances increase by 86%.2

For illustrative purposes only. Past performance does not guarantee future results.

New contributions can take advantage of potentially attractive pricing as the markets recover.

Historically, market rebounds are concentrated in a few distinct spurts. We expect the market to rebound again, but we can't know exactly when that will happen.

Performance is hypothetical for the period from 3/2/2000 to 2/28/2020 and for illustrative purposes only. Past performance does not guarantee future results.

Consider the above chart, which shows the hypothetical return of $100K invested in the S&P 500 Index from March 2000 to February 2020 (yellow bar). To the right, you can see the impact of having missed top-performing days. Staying invested earned more than double that of the portfolio which missed the top 10 performing days.

Here are some actions you may want to consider taking - and avoiding – when markets are volatile.

We recognize that those who are experiencing significant and immediate financial distress may need to turn to their retirement plan for relief.

For those thinking about taking this course of action, here are some things to consider in advance:

In financial markets, volatility refers to the extent to which the price of an asset or market index changes over time. It essentially describes how much and how quickly prices fluctuate.

In a volatile market, your 401(k) investment, especially those heavily in stocks, are likely to experience fluctuations. While this can cause concern, consider whether to avoid panic selling and focus on long-term strategies like diversification and continued contribution.

If you withdraw money from your 401(k) before age 59.5, the IRS generally assesses a 10% penalty in addition to the regular income tax on the withdrawal. The withdrawal is treated as taxable income, and you’ll pay federal income tax at your ordinary income tax rate.

Learn how to avoid some common pitfalls when it comes to saving for retirement in a volatile market.

1. Source: Morningstar. Returns are principal only not including dividends. Stocks are represented by the S&P 500 Index, an unmanaged index that is generally considered representative of the U.S. stock market. Past performance is no guarantee of future results. For illustrative purposes only. It is not possible to invest directly in an index.

2. Investment Company Institute, “What Does Consistent Participation in 401(k) Plans Generate? Changes in 401(k) Account Balances, 2007-2013.” The average 401(k) account balance for consistent participants fell 25.8 percent in 2008, then rose from 2009 through year-end 2013. Overall, the average account balance increased at a compound annual average growth rate of 10.9 percent from 2007 to 2013, to $148,399 at year-end 2013.

This material is provided for educational purposes only and is not intended to constitute investment advice or an investment recommendation within the meaning of federal, state or local law. You are solely responsible for evaluating and acting upon the education and information contained in this material. BlackRock will not be liable for direct or incidental loss resulting from applying any of the information obtained from these materials or from any other source mentioned. BlackRock does not render any legal, tax or accounting advice and the education and information contained in this material should not be construed as such. Please consult with a qualified professional for these types of advice.

Prepared by BlackRock investments LLC, member FINRA.

No part of this material may be reproduced, stored in any retrieval system or transmitted in any form or by any means, electronic, mechanical, recording or otherwise, without the prior written consent of BlackRock. This publication is not intended for distribution to or use by any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation.

The opinions expressed in third party articles or content do not necessarily reflect the views of BlackRock. BlackRock makes no representation as to the completeness or accuracy of any third-party statement.

©2026 BlackRock, Inc or its affiliates. All Rights Reserved. BLACKROCK and READ ON RETIREMENT are trademarks of BlackRock, Inc. or its affiliates. All other trademarks are those of their respective owners.

MKTG0526-5483293-EXP0527