Productivity Slowdown Puzzle

27 Jan 2016

Labour productivity has slowed sharply around the world. Why does this matter? Productivity is the key driver of potential growth rates and living standards in the long term. We dove into the possible reasons for sluggish productivity growth and its implications for monetary policy, asset prices and corporate capital management. Highlights:

- A productivity revival is crucial for getting ailing economies back on their feet. Productivity trends in coming years, we believe, will have a more far-reaching impact on economies and asset prices than market fixations such as how much the US Federal Reserve (Fed) raises interest rates in 2016 – or whether the European Central Bank will ease policy more. Productivity will be a major driver of policy decisions in the long run, in our view.

- The causes of the productivity slowdown vary across regions. A recent slowdown in capital expenditures (capex) per worker is the major driver in the developed world. A long-term slump in total factor productivity (a proxy for technological innovation) is exacerbating the trend. The latter is the main driver in emerging markets (EMs). This adds to current EM challenges such as China’s economic slowdown and the commodity price crunch.

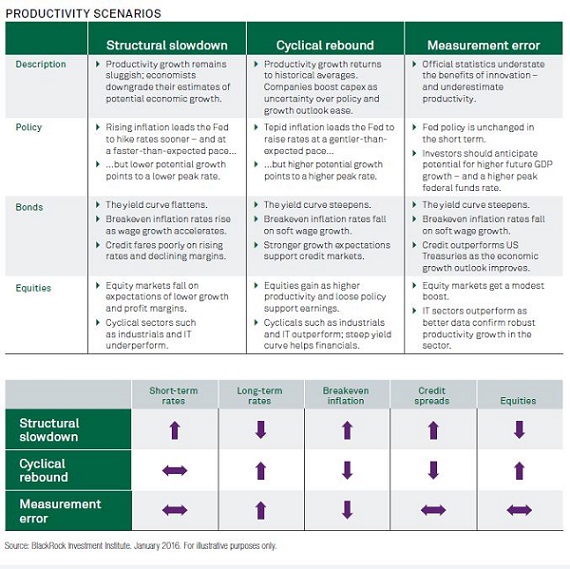

- We introduce three productivity scenarios with different implications for economies, policy and asset prices: 1) Structural Slowdown: productivity stays low as the benefits of today’s innovations pale against those of the past (think electricity); 2) Cyclical Rebound: productivity growth rebounds as economies recover, rates rise and companies boost capex; 3) Measurement Error: official data underestimate the benefits of new innovations.

- We think all three scenarios are at play to some extent, but we lean toward Measurement Error. Innovation is changing business so fast that traditional economic metrics simply have not kept up. Many technologies are bringing greater efficiencies at lower cost. When we consider the quality improvements and downward influence on prices of innovation, consumption and productivity growth look much better than official data would suggest.

- Productivity ties in with the debate on what companies should do with their cash. Share buybacks have become the favoured use of capital amid low rates. Buybacks and research and development (R&D) spending have delivered the highest shareholder returns in US markets since 1985, our analysis shows. The results for capex were mixed; cash acquisitions, dividends and debt reduction led to shareprice underperformance, we find.

In Singapore, this material is issued by BlackRock (Singapore) Limited (company registration number: 200010143N). Investment involves risks. Past performance is not a guide to future performance. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader. This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. Any opinions contained herein, which reflect our judgment at this date, and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. This material is for informational purposes only and does not constitute an offer or invitation to anyone to invest in any BlackRock fund and has not been prepared in connection with any such offer. Any research in this material has been procured and may have been acted on by BlackRock for its own purpose. The results of such research are being made available only incidentally. BlackRock® are registered trademarks of BlackRock, Inc. All other trademarks, servicemarks or registered trademarks are the property of their respective owners. © 2016 BlackRock Inc. All rights reserved. (S0116-121)

Views on the UK vote to leave the European Union

Read it now

Impact investing is playing an increasing role

Read it now

Aging populations provide long-term support

Read it now

Insights on Markets and Investment Guidance

Read it now