BlackRock Asia Weekly Market Views

3 Nov 2015

Click here to see our latest Portfolio Manager views

Weekly Highlights

- Total returns on Asian credit was flat over the past 2 weeks with positive spread returns compensating for negative returns due to higher US treasury yields. Credit spreads continue to compress as the prospect of more monetary stimulus from the European Central Bank providing a lift on risk assets.

- Asian credit was further supported after further monetary easing by the People’s Bank of China which included not just cuts to benchmark rates but also cuts to the reserve requirement ratios. While the October statement from the FOMC was hawkish and led to higher US treasuries (negative treasury return), credit spreads were negatively correlated to US treasury yields and average yields on Asian credit remained stable. High yield outperformed investment grade overall with the demand for yield unabated. The better market sentiment boosted new issuance but the supply picture continues to underwhelm, providing a strong technical support for Asian credit.

- The divergence in global rates and central bank action continues to play out in the FX markets. With major Asian central banks in easing mode, Asia currencies weakened against the US dollar. Average bond yields were marginally higher but income from bond coupons made up for any negative returns due to that. The exception was renminbi bonds which saw positive returns against the US dollar as yields moved lower post the cuts to the benchmark rates and reserve requirement ratio. In addition, the renminbi remains quite stable against the US dollar with continued convergence in the onshore and offshore exchange rates. Despite the weaker performance in US dollar terms, Asian local currency bonds performed well in Euro terms with Asian currencies appreciating against the Euro.

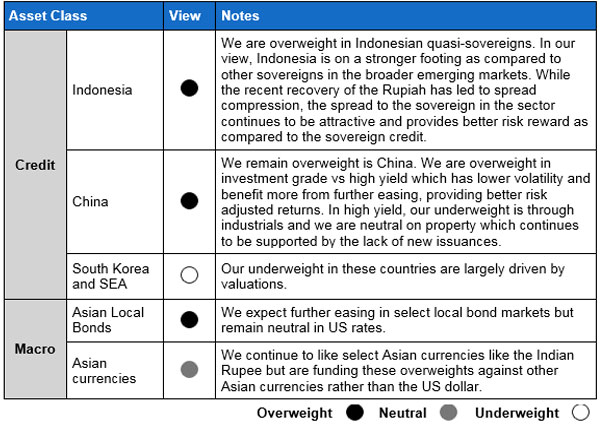

Country views from the BlackRock Asian Fixed Income Team

In Singapore, this material is issued by BlackRock (Singapore) Limited (co. registration no. 200010143N). For informational or educational purposes only. Investment involves risks. Past performance is no guarantee of future results. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader. International investing involves additional risks, including risks related to foreign currency, limited liquidity, less government regulation and the possibility of substantial volatility due to adverse political, economic or other developments. The two main risks related to fixed income investing are interest rate risk and credit risk. Typically, when interest rates rise, there is a corresponding decline in the market value of bonds. Credit risk refers to the possibility that the issuer of the bond will not be able to make principal and interest payments. This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. All data in this communication is sourced from Bloomberg/Thomson Reuters/Datastream as of November 3, 2015 and the opinions expressed are as of November 3, 2015 and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. There is no guarantee that any forecasts made will come to pass. They do not necessarily reflect the views of any company in the BlackRock Group or any part thereof and no assurances are made as to their accuracy. Index performance is shown for illustrative purpose only. You cannot directly in the index. Company name is only for explanatory purposes and does not constitute as investment advice and is subject to change. Any investments named within this material may not necessarily be held in any accounts managed by BlackRock. ©2015 BlackRock, Inc. All Rights Reserved. (S1115-14)

China has been in news over the past two weeks.

Read it nowIndia’s budget priorities unveiled

Read it nowRegional credit posts better week

Read it nowGrowing intra-regional divergence

Read it now