Your ability to tolerate risk can help be determined by two key factors:

- Willingness to take risk: This refers to how well you can stomach market volatility. Do market gyrations cause you emotional angst?

- Ability to take risk: This refers to your financial capacity to take risk and is based on time horizon and liquidity needs.

Shorter-term goals (e.g. vacations, emergency funds) may require a more conservative investing approach, with a focus on safety and preservation of capital. Consider high quality bonds, such as short-term investment-grade bonds, which typically carry a lower risk of default and exhibit less volatility compared to riskier assets.

Medium-term goals (e.g. down payment on a home, college education) typically allow for a higher tolerance for investment risk. With more time to recover from market fluctuations, allocating a portion to equities could help your investments grow more than investing in bonds alone.

Long-term goals (e.g. retirement or estate planning) can span decades, allowing you to consider investments with higher potential risk and return profiles. Examples include less liquid assets such as real estate that require longer holding periods.

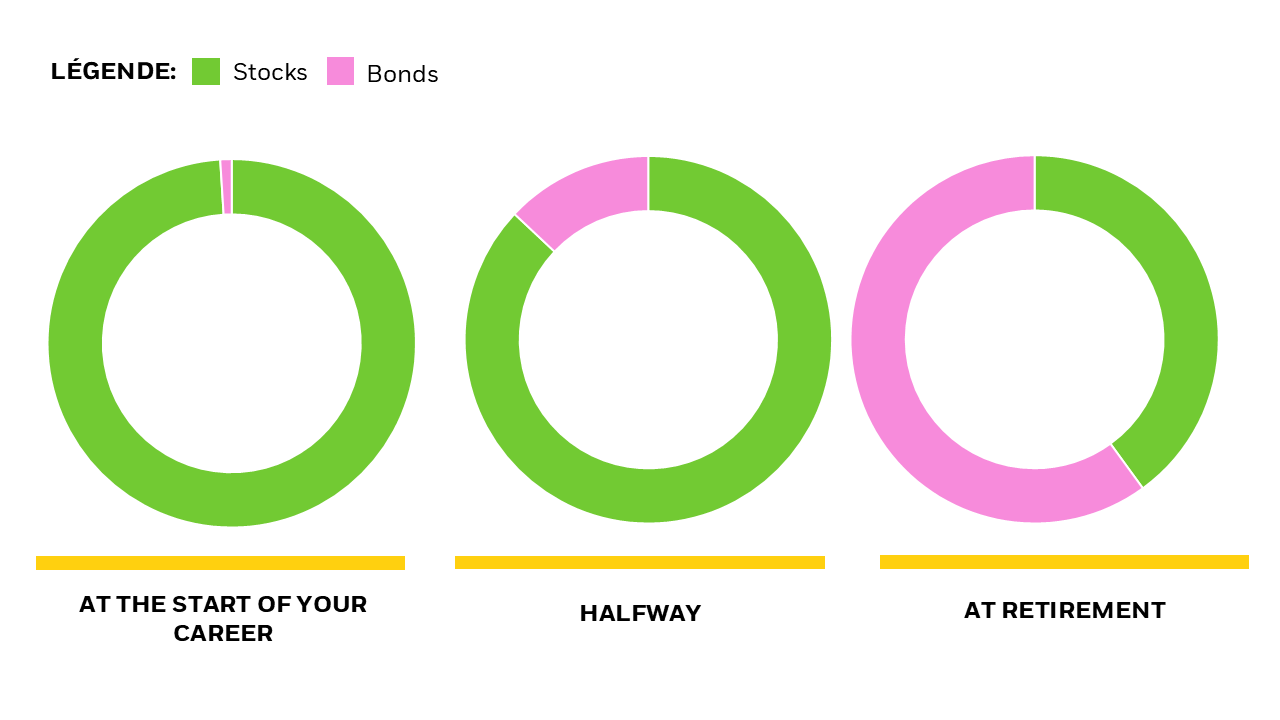

Importantly, the further away you are from your financial goal, the more time you have in the market to grow your assets and recover from any near-term losses, typically allowing for a greater risk tolerance.