More people should get to grow with their country. We serve clients in more than 100 countries—helping individuals invest for retirement, helping economies deepen their capital markets, and helping connect the two. Here's what that work looked like over the past year.

BlackRock entered 2026 from a position of strength: record flows, double-digit organic base fee growth in the fourth quarter, a new assets under management (AUM) high of $14 trillion, and a platform that is unified, integrated, and relevant for today’s opportunity set. We help clients navigate change and invest with confidence, creating enduring value for them and for you, our shareholders. The growth investments we’ve made to align our platform with the biggest opportunities for clients are resonating through significant client engagement and accelerating activity across our platform.

2025 marked the strongest year of net inflows in our history, as clients entrusted BlackRock with nearly $700 billion of net new assets. 2025 organic base fee growth of 9% represented $1.5 billion of net new base fees. And our results stand out even more over the long term, with $2.5 trillion of net inflows in the last five years helping to drive a more than 60% increase in AUM.

All of this growth took place as we executed on our largest integrations in more than 15 years, with our acquisitions of HPS, Preqin, and ElmTree closing in 2025, following the acquisition of GIP in 2024. We’re now a scale operator across public and private markets and technology. That’s significantly enhancing our positioning with clients worldwide.

Our pipeline of business has broadened across products and regions, spanning public and private markets mandates, technology and data, and client channels. We’re seeing excellent fundraising activity. We have an ambitious 2026 fundraising plan diversified across infrastructure equity and debt, private financing solutions, and multi-alternatives as we progress toward our goal of $400 billion in private markets gross fundraising by 2030.

Whether in private markets, technology, or ETFs, size and scale are outputs of performance. BlackRock has wrapped a successful 2025, and now we’re moving with speed and momentum to drive upward from here.

BlackRock shareholders are one of the biggest beneficiaries of our growth. We returned a record $5 billion to shareholders in 2025 through a combination of dividends and share repurchases. Our conviction in our model and the durability of our cash flow led us to raise our 2026 dividend per share by 10%, alongside an increase in our planned share repurchases. We know that dividend income is important to many of our shareholders, including those in retirement. We’re proud to have delivered a 10% compounded annual growth rate on our dividend in the last ten years alongside a 15% annualized return on share repurchases.

Our results in 2025 were not driven by a single market or product. They reflected broad-based momentum, and a business model designed to evolve alongside the markets. ETFs continued to demonstrate their role as core building blocks for portfolios worldwide. Active strategies were used to help deliver alpha, income generation, and diversification. Private markets saw growing demand as investors sought income, diversification, and long-duration growth. And Aladdin reinforced its position as valuable enterprise technology, supporting better decision-making for clients navigating more complex markets.

Just as importantly, we continued to grow with discipline. We invested in our people, our technology, and our global footprint while delivering premium margins through operating leverage inherent in our model. Scale at BlackRock is not an abstraction—it is what allows us to invest continuously while keeping costs down for clients and creating durable value for shareholders.

iShares remains a growth engine for the firm, delivering another record year in 2025 with $527 billion of net inflows. We’re seeing significant momentum across our premium growth categories, like active ETFs, digital assets, and international markets. We led global ETF flows in 2025, and our organic revenue was more than triple the next largest issuer’s. We’ve already had a strong start to 2026, with $103 billion in iShares net inflows through the end of February. Those flows are nearly double what they were at this point in 2025, which is great to see. But what’s even more inspiring is the global reach and diversification of activity across premium value categories.

Our $2.5 trillion active franchise continues to deliver meaningful alpha for clients and strong organic growth, even against a backdrop of industry outflows. Our fundamental fixed income platform generated over $45 billion of net inflows in 2025, continuing to outpace industry growth. We’re working across the spectrum of fixed income opportunities, from municipals to high yield, to total return and unconstrained. And in active equities, our systematic platform raised more than $50 billion in 2025, powered by the machine learning and big data capabilities we’ve been developing for more than two decades.

In private markets, we’re executing on an ambitious fundraising plan to raise a cumulative $400 billion by 2030. We have scaled platforms across two of the fastest-growing sectors in private markets—infrastructure and private credit. And we’re executing on a growing opportunity to bring the benefits of private markets investments to more investors, including insurance and wealth clients, and individuals saving for retirement.

In infrastructure, we closed GIP’s fifth flagship fund at $25.2 billion, representing the largest-ever client capital raise in a private infrastructure fund. And our AI Infrastructure Partnership is supporting the growth of artificial intelligence through investment in new and expanded AI infrastructure, including through its recent agreement to acquire Aligned Data Centers. In private credit, we saw nearly $20 billion of net inflows in 2025, primarily led by HPS’ flagship franchises. We have a strong fundraising and deployment roadmap ahead for 2026 and beyond.

Clients are deepening their work with BlackRock, in larger and more innovative ways than ever before. In 2025, we onboarded $80 billion of separately managed accounts (SMA) assets in connection with our Citi Wealth mandate, alongside several other scaled outsourcing assignments throughout the year. Importantly, we’re seeing demand for these solutions from clients of all types, from scaled institutional partners to endowments, healthcare organizations, and family offices. It’s our comprehensive, global platform that allows us to meet our clients’ portfolio needs, across public and private markets asset classes, across regions, and through active and index, all supported by our Aladdin technology.

One of BlackRock’s enduring strengths is that we operate as a truly global asset manager, while remaining deeply local in how we serve clients. We’re playing a role in the transformation of the capital markets around the world, including in countries where people are just beginning to invest their hard-earned savings. In India, our joint venture JioBlackRock now manages funds for nearly 400 institutions and more than a million retail investors. Our strong local presence also translates to meaningful revenue growth for BlackRock and our shareholders, with Latin America, the Middle East, and Asia all delivering double-digit organic base fee growth last year.

Technology is central to how we scale globally and deliver durable growth, and Aladdin sits at the core of that strategy. In 2025, we closed our acquisition of Preqin, tripling our desktop reach with clients and expanding our public and private markets workflow offering into the fast-growing private markets data space. We closed the year with 16% organic annual contract value (ACV) growth.

We’ve always seen Aladdin as the language of portfolios. Today, institutional clients around the world are turning to Aladdin to simplify their investment operations or integrate their data, risk, and portfolio management capabilities into a single, unified platform. For shareholders, our technology both supports BlackRock’s growth and generates long-dated, recurring revenue for BlackRock. This model reinforces operating leverage and deepens client relationships. It positions BlackRock at the center of the blending of public and private markets, data and investing, and technology and advice.

BlackRock’s platform is anchored by scale engines tied to the long-term expansion of the global capital markets and fast-growing client and product channels. The opportunity ahead is inspiring: to help reshape portfolios for more complex markets, deepen partnerships with clients, and deliver durable, profitable growth for our shareholders. We enter 2026 with the combined strength of BlackRock, GIP, HPS, and Preqin—now all One BlackRock—and we’re excited to share our growth with clients, employees, and shareholders.

Executing on our 2030 ambitions

At our 2025 Investor Day, we communicated our ambitions for BlackRock in 2030. We’ve established strength at the foundation of our platform in ETFs, Aladdin, whole portfolio, fixed income, and cash management. They’re the strong foundations to serve clients and deliver on our organic growth objectives.

We also executed on organic business builds in structural growth categories, including digital assets, active ETFs, model portfolios, and systematic equities.

Looking ahead to 2030, we aspire to deliver more than $35 billion in revenue, with 30% or more coming from private markets and technology. We expect the increase in revenue to be underpinned by our goals of 5% or greater organic base fee growth and low-to-mid-teens technology ACV growth. We’re aiming to nearly double adjusted operating income from 2024, alongside 45% or greater adjusted operating margins through the market cycle. We already have industry-leading margins, and we see opportunity to drive margin expansion through the fee-related earnings growth trajectory of private markets and our highly scaled foundational businesses. And all of these goals assume a flat market environment, with meaningful upside if markets are even modestly positive on the road to 2030.

BlackRock’s growth in 2025 was broad-based across capabilities that we’ve had for decades and others that we’ve built or acquired in the last two years. We expect a similar path to 2030, with growth coming from both our strong foundational pillars—like iShares and Aladdin—and franchises that we’re building in newer, high-growth markets across the industry. Private markets to insurance, private markets to wealth, digital assets, and active ETFs—we think these can all be $500 million revenue generators in the next five years.

We see a sizable opportunity to bring private markets to more investors, which can serve as a portfolio enhancer with diversification from the public markets, alongside long-term growth and income potential. Our investments in infrastructure, private credit, and alts-to-wealth ground our ambition to raise $400 billion in private markets by 2030. BlackRock already manages $3 trillion on behalf of insurance, wealth, and outsourcing clients. We have a significant opportunity to deliver better outcomes and experiences for clients in their private markets allocations.

For example, BlackRock is the largest insurance general account manager,40 with $700 billion of assets. With HPS, we’re now also a scaled provider of asset-based finance and high-grade private debt offerings. We’re already seeing early momentum to bring high-grade private debt into portfolios that have historically invested with us in public markets.

And in wealth, we already have a strong presence, with over $30 billion in retail private markets AUM, alongside BlackRock’s global distribution platform and comprehensive advisor relationships. We’re now extending our private markets to wealth offering into a broader set of products and multi-alternatives models. We also recently launched a first-of-its-kind private markets SMA solution with Partners Group to enable greater retail access to private equity, private credit, and real assets. Delivered through a single subscription document, the strategies are designed to meet client objectives while minimizing operational complexity for advisors and their clients. These collective offerings are an important step to bring the benefits of private markets to more investors, including those saving for retirement or other financial goals.

BlackRock has long advocated for a broadening of retirement savings, whether through investment accounts seeded at birth or enabling more individuals to shift from savers to investors within the capital markets. More than half of our $14 trillion in AUM is linked to retirement, whether for an individual investor through an ETF or 401(k), or for pension clients investing on behalf of millions of schoolteachers, firefighters, and union workers around the world.41

We’re the largest defined contribution investment-only manager,42 which includes more than $600 billion across our LifePath target-date offering. Our LifePath Paycheck innovation pairs the flexibility of a target-date fund with a solution designed to give workers access to income streams they can rely on in retirement.

Many retirement plans around the world, including defined benefit plans, already include private markets allocations, bringing diversification, income, and the potential for greater alpha to individual constituents, not just institutions. But in the United States, the vast majority of retirement savers access the capital markets through a 401(k) offering, and don’t have access to private markets. We’re seeing significant momentum for a regulatory framework that could change that. We believe that private markets offer the potential to enhance retirement outcomes for participants when thoughtfully and responsibly incorporated into a professionally managed target date fund. Changes that bring private markets into 401(k) plans represent another opportunity for Preqin. Plan sponsors will need a wealth of data and standardized benchmarks, and Preqin is well-positioned to help provide this data and accelerate the transition.

Earlier this year, we unified Preqin’s data onto Aladdin. With Aladdin, eFront, and Preqin, we’ve created a public and private workflow and data solution housed within a single platform. I believe Aladdin will be a major beneficiary of AI, enabling clients to work with greater efficiency across ever-growing data sets and to unlock scale in their investment and analysis processes. AI can be a powerful business accelerator for Aladdin, amplifying the strengths of its scale, deep resources, proprietary data, and extensive embedded network across the global investment ecosystem.

BlackRock is also actively building in exciting newer technologies in financial markets, including digital assets and tokenized funds. Today, there’s very little access to traditional investment products in digital wallets. We plan to lead the charge in changing that.

BlackRock has already established early leadership in bringing institutional-quality products to the digital markets at scale, with nearly $150 billion in AUM connected to digital assets. Our tokenized treasury fund has grown into the largest tokenized fund in the world, and we manage $65 billion of stablecoin reserves, alongside nearly $80 billion of digital asset exchange-traded products (ETPs).43 We’ve built all of these franchises in just the last few years, and we’re studying opportunities to grow our position even further.

Our digital assets ETPs are another example showing how our iShares ETF platform remains a powerful center for growth and innovation, generating double-digit organic asset and base fee growth in 2025. Even at more than $5 trillion in AUM, iShares is still unlocking new use cases for ETFs, bringing new investors into the capital markets and expanding our reach across regions.

In addition to digital assets, active ETFs represent an emerging growth channel for iShares. Our active ETF platform tripled in size in 2025, ending the year at nearly $100 billion in AUM with significant runway ahead. Our clients are increasingly embedding active ETFs into their portfolio strategy, including models, to unlock alpha, manage downside risk, or generate ongoing income. We’re bringing our active capabilities into the ETF market, broadening access to our portfolio managers and alpha opportunities to more investors around the world.

In Europe, we’re capitalizing on an expanding market, as a wave of first-time investors begins to enter the capital markets through monthly savings plans and digital-first offerings. 2025 iShares net inflows in Europe were 50% higher than 2024, capturing more than a third of flows in the region. We’re executing on a strong opportunity to build our business here, and across the world, as the ETF vehicle gains traction with individuals and institutions alike.

For shareholders, our 2030 strategy is designed to deliver higher, more durable growth and increasing margins over time. As we scale businesses with strong secular tailwinds and recurring revenue, we expect more consistent organic growth, improved earnings resilience through market cycles, and meaningful long-term value creation. Our diversified platform, disciplined capital allocation, and focus on execution position BlackRock to compound earnings while continuing to invest for the future. This alignment between client success and shareholder outcomes is at the core of our strategy, and why we believe the BlackRock we are building for 2030 is stronger, more resilient, and better positioned than ever.

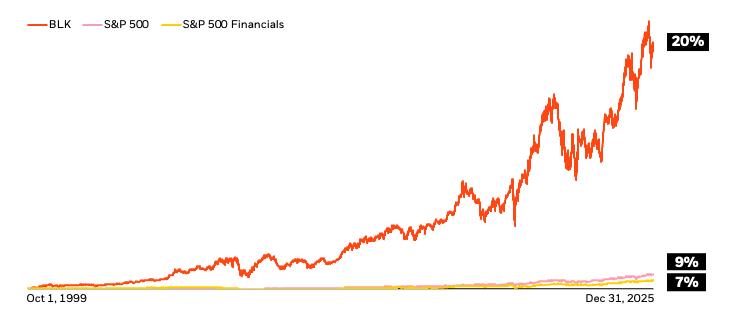

Total compounded annual total return since BlackRock’s IPO through December 31, 2025

The power of our integrated platform and strength of our relationships with our clients are key sources of the differentiated returns we’ve delivered for our shareholders. Since our IPO in 1999, we’ve generated an annualized total return of 20%, compared to 9% for the S&P 500 and 7% for the financials industry.

Source: S&P Global as of December 31, 2025. The performance graph is not necessarily indicative of future investment performance.

Our growth and success begin with our world-class talent, and our leadership team is no exception. In 2025, we expanded our Global Executive Committee to include more emerging enterprise leaders who will help advance our strategy in the years ahead. And in the last 18 months, we’ve welcomed an outstanding group of leaders from GIP, Preqin, and HPS. We have a long history of successful integrations, and a number of our current senior leaders joined us through acquisitions. We’re already benefiting from the fresh perspectives and experience of our new colleagues alongside our homegrown talent.

Our Board of Directors

BlackRock’s Board has long been an essential component of BlackRock’s growth and success. Their deep knowledge and strategic insight help shape our long-term strategy and inform the decisions that position us for the opportunities and challenges ahead.

Earlier this year, our Board appointed Gregg Lemkau, Co-Chief Executive Officer of BDT & MSD Partners. Gregg brings a wealth of experience in the financial services industry, and I believe his perspectives will be invaluable as we execute on the next phase of our growth.

Looking ahead

Today, BlackRock is positioned at the intersection of the most powerful forces reshaping global finance: the long-term growth of the capital markets, the modernization of portfolios, the expansion of private investment, the evolution of AI, and the digital transformation of investing itself. Our diversified platform means we can meet clients wherever market opportunities align with their portfolio objectives—and do so profitably, responsibly, and at scale.

This is why we believe it is a compelling time to be a BlackRock shareholder. We enter 2026 with strong organic growth, a resilient earnings base, and multiple structural tailwinds working in our favor. Our strategy is clear. Our balance sheet is strong. And our purpose—to help more people experience financial well-being—continues to guide how we grow.

BlackRock has always been built for the long term. The results of 2025, and the momentum we’re seeing today, reinforce our confidence in the years ahead.