Some people think that index funds are managed by computers. In reality, a lot of work gets done behind the scenes by skilled portfolio managers.

For example, during index rebalances and reconstitutions—reweighting and deleting or adding securities, respectively—index fund managers must rebalance or reconstitute their portfolios accordingly.

While indexes assume an immediate, frictionless, and costless implementation of changes, index fund managers are faced with transaction costs, risks, and other frictions when they execute trades in their portfolios.

At the same time, when trading around index events, index fund managers have control and exercise discretion in seeking to track the index and maximise shareholder value.

This means that index fund managers must review information about upcoming index changes and have an implementation plan in place to buy or sell securities to align their portfolio with the index in a way that balances risk, return, and cost.

Other responsibilities may include tracking corporate actions that can impact the composition of an index, reinvesting dividend or interest payments received from a fund’s portfolio holdings, and monitoring risk in their portfolios and in the market.

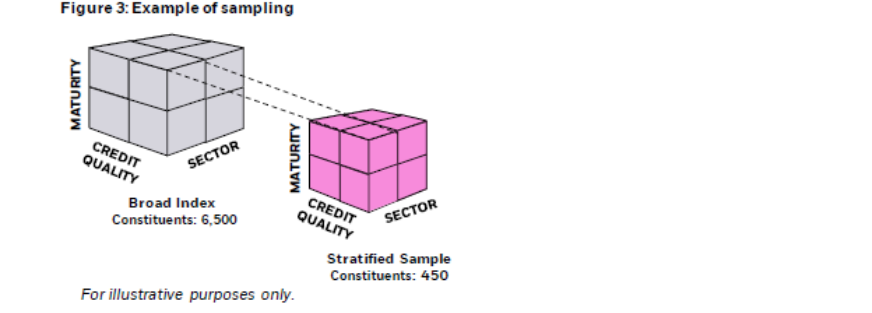

In instances where a portfolio holds a sample of an index’s securities, portfolio managers have discretion over security selection and can choose which securities to add or remove from the portfolio in order to continue tracking the index while aiming to minimise transaction costs and taxes.