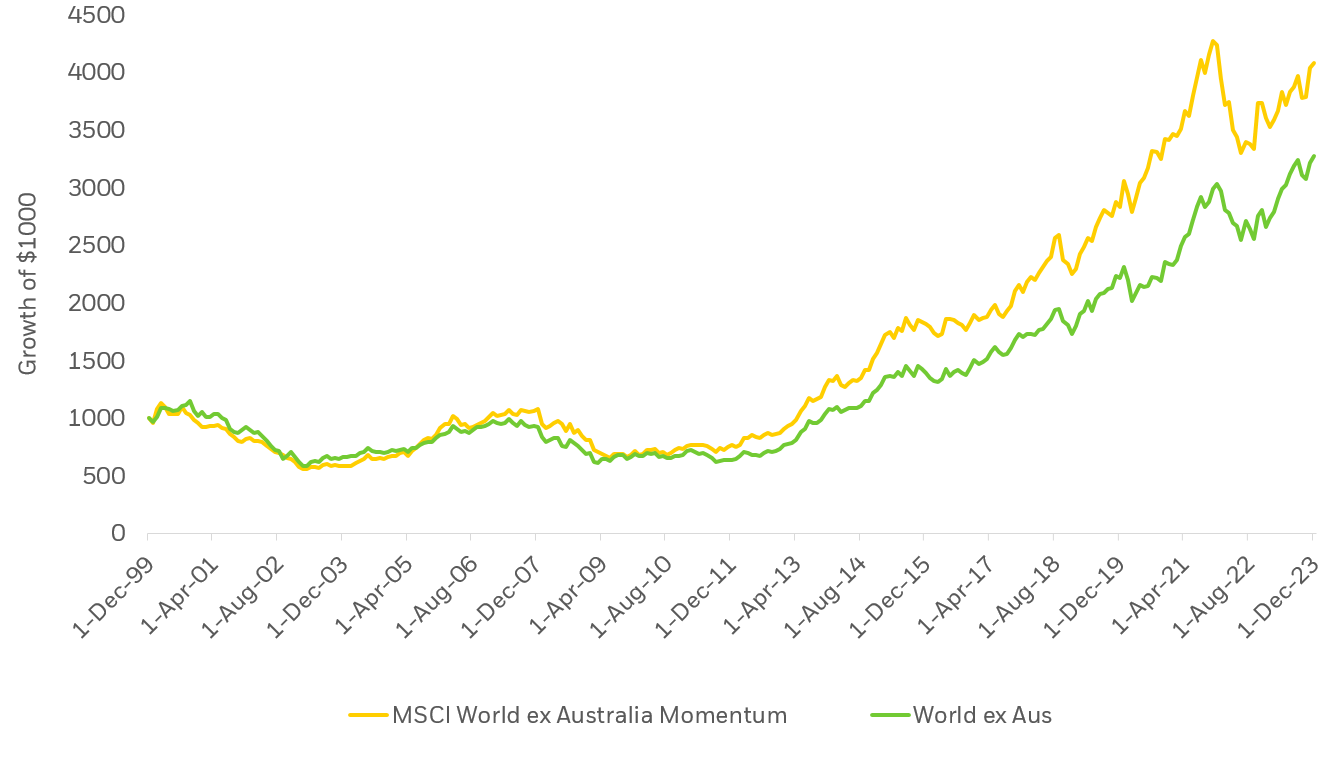

OUR APPROACH TO MOMENTUM INVESTING

The momentum index takes into consideration the relative risk-adjusted performance of each stock over the past 6 months and 12 months. Once identified, the top 30% of the parent universe with the strongest momentum exposure is selected (subject to some constraints – see below).