- Yields are back across all fixed income sectors with significant implications for advisors and their clients

- Advisors have an opportunity to rethink their clients’ overall asset allocations, and the tools they use to build their fixed income portfolios.

- Bond ETFs have gained widespread adoption as an instrument of choice to access attractive yields while simultaneously helping to reduce risk in portfolios.

Yields are back and it may be time to rethink your allocation

Apr 13, 2023

KEY TAKEAWAYS

The opportunity in fixed income may be nothing short of profound.

After last year’s relentless selloff in bonds, yields are back across all fixed income sectors. The swift repricing unleashed billions of dollars of fixed income assets in 2022, much of which migrated to bond ETFs1 as investors sought to reduce risk and recalibrate portfolios to attractive yield levels. The market conditions of last year may have functioned as a high-octane accelerant for bond ETF adoption as investors likely prized the transparency, access, liquidity and efficiency of these products during the market tumult.

In our opinion, the seeds of 2022’s bond market rout were sown in the Great Financial Crisis and its aftermath. Because the Federal Reserve left rates so low for so long after the Crisis, investors were forced to “reach for yield” in sectors such as high yield or lower-quality securitized assets to generate even modest income.

Meanwhile, concerns about the strength of the financial sector in March led to a rally in bonds, a traditional “flight to quality” reasserting the potential diversification advantages of fixed income in times of market turmoil. Advisors now have an opportunity to not only rethink their clients’ overall asset allocation, but the tools they use to build the fixed income portion of those portfolios. The fact that yields are back to the highest levels in 15 years (see Figure 1) may have major implications for clients who can finally look to bonds again for possible income and potential diversification benefits.

YIELDS ARE BACK

With inflation soaring and the Federal Reserve aggressively hiking rates, in 2022 the S&P 500 lost 18% and the Bloomberg U.S. Aggregate Bond Index fell over 13%,2 making it the worst year for 60/40 portfolios3 since 2008.

However, investors may now have an opportunity to earn much higher yields across sectors and maturities. From 2013 to 2021, only emerging market and high yield debt provided yields over 4%; now, over 70% of fixed income sectors are yielding 4% or greater. (Figure 1). This represents a huge shift in the investing landscape.

Source: BlackRock Investment Institute, Bloomberg and Thomson Reuters, 2/28/2023. The bars show market capitalization weights of assets with an average annual yield over 4% in a select universe that represents about 70% of the Bloomberg Multiverse Bond Index. U.S. treasury represented by the Bloomberg U.S. Treasury index. Euro core is based on the Bloomberg French and German government debt indexes. U.S. agencies represented by Bloomberg U.S. Aggregate Agencies index. U.S. municipal represented by Bloomberg Municipal Bond index. Euro periphery is an average of the Bloomberg Government Debt indexes for Italy, Spain and Ireland. U.S. MBS represented by the Bloomberg U.S. Mortgage Backed Securities index. Global credit represented by the Bloomberg Global Aggregate Corporate index. U.S. CMBS represented by the Bloomberg Investment Grade CMBS index. Emerging market combines the Bloomberg EM hard and local currency debt indexes. Global high yield represented by the Bloomberg Global High Yield index. Past performance is no guarantee of future results. Index performance is shown for illustrative purposes only. You cannot invest directly in an index.

FIX THE “40”

We estimate most investors are still under-allocated to fixed income. Our recent survey of advisors shows the average 60/40 portfolio was underweight fixed income by 9%.4 The upshot may be an opportunity for advisors to reallocate client assets to fixed income. In the process, many investors can reduce equity over-weights, and possibly move up in credit quality and liquidity, all while seeking diversification and a reduction of aggregate portfolio risk.

Historically, investors may have solved for the 40% allocation by allocating to a single manager / single fund. If the manager happened to be pursuing a strategy that became highly correlated with equities, it could lead to even greater portfolio underperformance during risk-off periods.

We believe the “active vs. passive” dichotomy is outdated. A robust approach would combine elements of active and index: using low-cost index components to create a more diverse and predictable exposure while also allocating to an active manager to pursue excess return.

As an example, in a multi-asset portfolio, an investor may choose to hold a combination of Treasury, agency MBS, investment grade and TIPS index ETFs as diversifiers against broad equity exposure while also holding an allocation to an unconstrained bond manager.

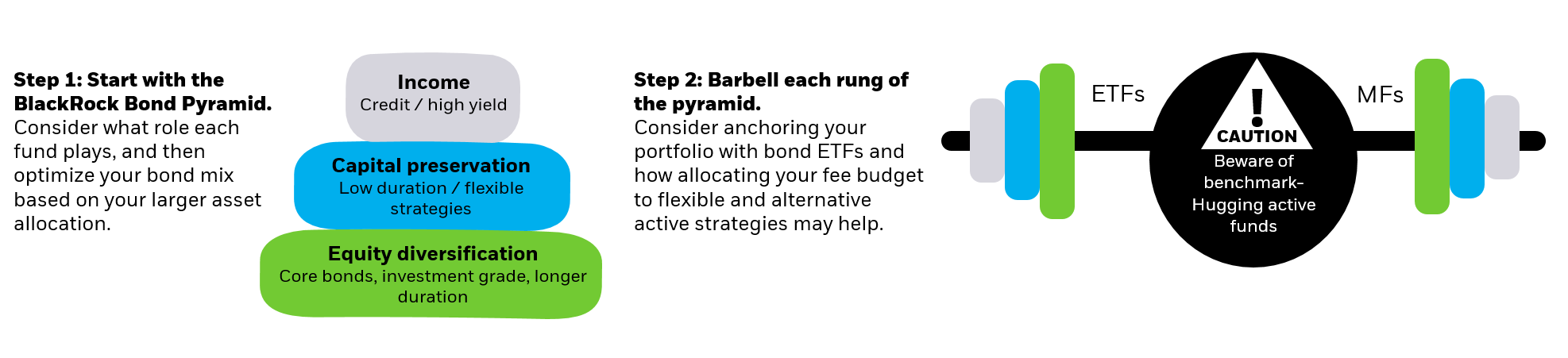

The “evolved 60/40 portfolio” may have the advantage of greater transparency and predictability in the 40% bucket through index building blocks, while still allocating to an unconstrained manager for potential alpha generation (ideally this manager would exhibit low correlation with the other portfolio components). In short, by combining building blocks and active strategies advisors can “barbell” their clients’ bonds.

To generate greater portfolio income, managers may tilt to sectors such as high yield or lower quality securitized assets. Unfortunately, such a strategy can result in the “40” becoming more positively correlated with equities as opposed to providing diversification. As a result, many managers underperformed last year. Over the most recent 3- and 5-year periods, the average fund in the Morningstar “core plus” category was 67% and 55% correlated with the S&P 500, respectively. For reference the Bloomberg U.S. Aggregate Bond Index was 50% and 36% correlated with the S&P 500 over the same period.5

Barbell your bonds in 2023

For illustrative purposes only.

BOND ETF ADOPTION ACCELERATES

The great paradox of 2022 was that in the midst of one of the most difficult fixed income markets in a generation, a torrent of assets came into fixed income ETFs. U.S. bond ETF inflows were approximately $200 billion6 while trading volumes were up 40% from the prior year7. In the face of abysmal returns, persistent volatility, and high inflation, investors of all types turned to bond ETFs to navigate this historically fraught market. Many investors also seized on a once in a decade opportunity to tax loss harvest, shifting from mutual funds to bond ETFs8.

With their liquidity, efficiency and breadth of exposures, bond ETFs have gained widespread adoption as an instrument of choice to access attractive yields while simultaneously helping to reduce risk in portfolios.

CONCLUSION

Although the confluence of forces shaping the bond market in 2022 may not soon be repeated, the long-term, structural drivers of bond ETF adoption remain firmly intact. This only reinforces our view that bond ETFs will continue to grow, reaching $5 trillion in assets globally by 2030 while further cementing their role as a central and important part of the bond market itself.

iSHARES FUNDS

Explore a range of iShares ETFs to meet your clients’ investing goals.

Subscribe for the latest market insights and trends

Get the latest on markets from BlackRock thought leaders including our models strategist, delivered weekly.

Please try again

RELATED RESOURCES

Access exclusive tools and content

Obtain exclusive insights, CE courses, events, model allocations and portfolio analytics powered by Aladdin® technology.