Model portfolios are an increasingly popular way for advisors to reduce the time needed to manage individual client portfolios. This way, advisors can spend more time growing their overall practice while providing existing clients with the benefits of a professionally-managed portfolio.

Although advisors may encourage clients to make the transition to model portfolios for these reasons, it’s not necessarily a straightforward task. One primary hurdle to transitioning clients to model portfolios is taxes, particularly in cases where clients need to transition assets from taxable accounts in which they have significant capital gains. Clients often do not want to absorb the sizeable tax bill that comes with making such a transition.*

Model portfolios gaining popularity

About $315 billion in assets followed model portfolios as of June 30, 2021. It is a “conservative estimate” after the number of reported model portfolios more than doubled from the previous year, according to a 2021 Morningstar study.**

It’s hard to track model portfolios, but with more than 2,100 model portfolios reported in the market to Morningstar, it shows that advisors already have access to model portfolios and are trying to make use of them.

Model portfolios are growing in popularity because they are professionally designed and managed. By outsourcing some management functions to a model portfolio, advisors can devote more attention to client conversations.

To transition or not?

At face value, transitions may appear to be an all-or-nothing decision at one point in time for clients. An advisor introduces the model portfolio, and the client either agrees or disagrees with the proposal.

If the client disagrees, we’ve found it’s often because the client either can’t or doesn’t want to handle the increased taxes it’d cost to make the change. Other times, it could be because the client wants to continue holding a security that isn’t in the proposed model.

Whatever the reason, for the advisor and for the client, there doesn’t seem at first to be many options.

Doing the math

In a technologically advanced world, there is a way today for the advisors to create more options.

For example, maybe a client is willing to pay some taxes now to transition to an advisor’s model portfolio, and open to paying more in the future to continue transitioning into the model portfolio. What would that cost?

Taxes are among the most operationally challenging variables to address in clients’ portfolios. We’ll show you a simple way to go about the calculations with technology, through a hypothetical example.

What do you do when you’ve reached a fork in the road?

Creating more choices for clients

One day, a prospect, Alfred Baker meets with an advisor.

Alfred’s current portfolio has concentrated stock positions that led him to deviate significantly from his stated risk appetite. The advisor hopes to win Alfred’s account by optimizing $3 million of allocations closer to a target model portfolio that aligns with his risk profile and goals.

But there’s an obstacle.

Alfred doesn’t want to liquidate the portfolio and move to the proposed model. If he did that, it would increase his short-term taxes. He’s sensitive to any short-term taxes. Plus, Alfred is a stock picker who has embedded taxable gains in his investments.

What would you do if you were the advisor? If you want to show Alfred it doesn’t have to be an all-or-nothing decision, you can use technology to calculate the tradeoffs. Alfred can decide how close to the model portfolio he wants to get and see how much it’d cost in taxes to get there.

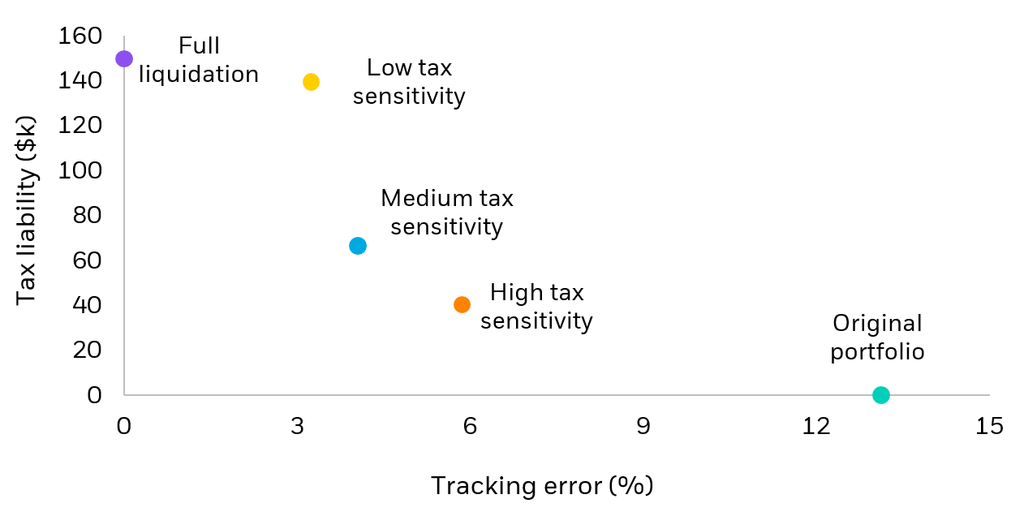

In the chart below, we visually represented the results.

Balancing the tradeoffs between taxes and tracking error

For illustrative purposes only. Based on data from BlackRock Aladdin, 2022.

Mapping a client course

As shown above, Alfred doesn’t have to fully liquidate or stay with his original portfolio. He has alternate paths for getting closer to the target portfolio – without having to stomach all the short-term taxes.

Understanding the tax tradeoffs can help lower the barriers for clients who are hesitant about making the transition to model portfolios. Even at a high tax sensitivity, as represented by the orange dot, the technology showed that the existing tracking error can be reduced by almost half while only incurring a fraction of the potential tax amount.

If you were the advisor, imagine the difference in conversation between an all-or-nothing approach compared to one with optionality. Which presentation would be more likely to convince Alfred to work with you?

Let’s say you present Alfred with the above choices. He decides to take the medium tax sensitivity path. You’ve now gained a new client and can help Alfred start the process of getting closer to the model portfolio.

Ongoing monitoring

Technology can also enable advisors to scale this for multiple clients. Advisors can monitor investments for clients on an ongoing basis, or over a specific time span.

Advisors can use this to continue determining how clients may further reduce tracking error as other opportunities arise, such as for tax-loss harvesting.

The challenging topic of taxes can become more digestible with technology, timely support for advisors as model portfolios continue to grow in popularity.

Aladdin Wealth™ as a compass

Using technology to help with tax management can enable advisors to personalize preferences that are specific to each client. On the Aladdin Wealth™ platform, advisors can optimize portfolios and calculate potential tax implications based on “tax-sensitivity” levels ranging from moderate to very high.

Advisors can also estimate tracking error to propose trades that can balance a client’s tax costs with portfolio risk, all while streamlining ongoing portfolio management processes. The platform provides more options for transitioning to model portfolios, so advisors don’t have to set out on new paths for clients without any help.