Impacts from market uncertainty, geopolitical events, monetary policy intervention by central banks and other types of macro shocks now carry greater weight in influencing markets compared to the past decade.

Scenario analysis can give you a potential glimpse at the future…

Applying forward-looking insights to the macroeconomic environment enables you to think about the full expanse of hypothetical investment outcomes.

Scenario analysis encourages portfolio and risk managers to think about what may happen in the future, not just focusing on evaluating what happened in the past to make more informed decisions.

But the future isn’t straightforward

The process of building a scenario analysis is as much an art as it is a science because there is no past anchor to serve as a gauge.

For this qualitative reason, the creation of hypothetical scenario analysis differs across the industry. Let’s delve into our version of scenario analysis, to show you the rigor that goes into the process of creating each one.

BlackRock’s Market-Driven Scenarios provide a solution

BlackRock originally developed our Market-Driven Scenarios (MDS) framework to mitigate the inherent subjectivity in modeling hypothetical outcomes.

The goal of MDS is to identify relevant market event risks, consider the range of potential economic and market outcomes around those risks, then analyze the hypothetical impact on portfolios across multiple variables at the same time.

Led by our Risk and Quantitative Analysis (RQA) team, we’ve spent years developing MDS across macroeconomic, geopolitical, and other policy themes. We strive to synthesize the best of BlackRock in our analysis by incorporating subject matter expert views across asset classes, geographies and skillsets.

From a critical lens, we focus on plausible market shocks. That means hypothetical scenario outcomes should represent a shift from the prevailing market environment, but they must also be sized according to our reasonable expectations for how markets could react to different shocks.

This process can involve comparing hypothetical shocks to previous market episodes, such as evaluating whether the event has a historical precedent or how extreme factor shocks appear relative to current market conditions.

Within the Aladdin Wealth™ platform, you can express market views across 3,000+ risk factors.

A brief case study

To give you an idea of the scenario development process, we’ll walk you through the way we think by showcasing what went into creating a MDS on potential policy changes by the U.S. Federal Reserve (Fed) in the face of heightened macro uncertainty. You’ll see the process flow chart below.

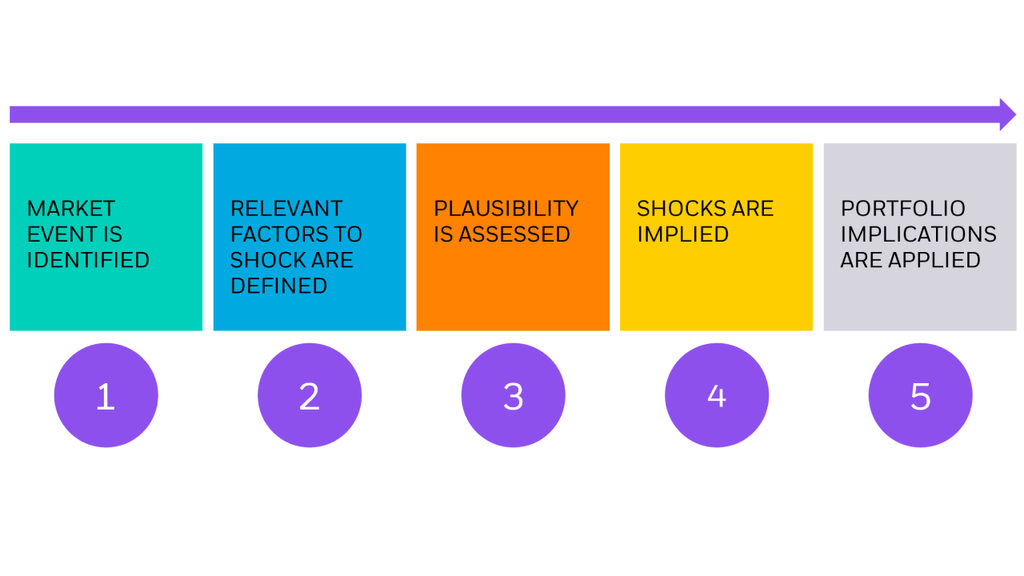

The BlackRock Scenario Analysis Lifecycle

Source: BlackRock. For illustrative purposes only.

Step 1: Defining the eventThe first step in any scenario build is to identify an event that you’d want to get ahead of in the market. Where could markets go? How could cross-asset correlations change? Scenarios can focus on macroeconomic regimes, geopolitical risks, sustainability or policy events.

For the Fed scenarios, we wanted to consider the Fed’s policy tradeoffs in the current environment by evaluating how the Fed could respond to incoming growth and inflation data during a turbulent market.

Step 2: Defining the scenariosThe next step in the process is to consider the range of potential outcomes around the event, which often includes a good, a bad, and an ugly case.

In the Fed MDS, we decided to consider two policy paths based on the elevated uncertainty of interest rates and high inflation, and how this uncertainty could affect portfolios.

In one path, we assumed that inflation would peak and begin to ease gradually because of a consumption shift from goods to services and diminishing global supply imbalances. In this scenario, the Fed would ease its hawkish stance, while markets would partially offset year-to-date losses.

For the second path, we assumed the Fed would be unable to execute a soft landing, as inflation pressures worsened from existing and potentially unforeseen supply shocks. In this scenario, a U.S. recession would follow, resulting in a significant extension of year-to-date losses.

Step 3: Assessing plausibilityAfter we defined the scenarios, we focused on explicit shocks to interest rates, inflation factors, commodities, and other risk assets that would be most impacted by a pivot in Fed policy.

Once market shocks are specified for each scenario, we compute implied shocks for all other relevant market risk factors based on historical correlations. We assess the plausibility of these results – meaning we evaluate how viable they are - and iterate as needed before finalizing the shocks for each scenario.

This process of adjustment and quantitative challenge is critical. It helps ensure that our scenarios are well-specified, and that the results are more likely to be stable through time.

Step 4: Implying shocksWhen the scenarios are finalized, we then imply what happens to remaining risk factors in the Aladdin® platform based on modeled relationships with the explicit shocks.

This step allows us to evaluate the market impact to factors that may not be the primary drivers behind a scenario but might still be affected. It can provide us with a more holistic view.In the Fed scenarios, for instance, we considered the potential impacts to currency factors that weren’t explicitly shocked on either the upside or downside case.

One essential part of this step is choosing an appropriate market economy date. The dates should reflect the environment portrayed in the scenario. We often choose the most recent economy date, but sometimes choosing a historical date could be more appropriate if it gives a better picture of the scenario’s intended cross-asset correlations.

For the Fed scenarios, we went with the most recent economy date because market moves were heavily swayed by concerns over inflation and Fed policy.

Step 5: Determining portfolio implicationsWhen the scenarios are live, they can be run against portfolios in the Aladdin® platform, yielding hypothetical scenario P&Ls based on a portfolio’s exposures. These impacts can be monitored on a regular basis for greater transparency into the portfolio’s most current risk exposures.

The goal of using MDS is to kickstart conversations about risk among wealth managers, advisors and their clients. It doesn’t provide the final portfolio decisions but can allow for greater transparency and insights along the way.

What we’ve learned from developing scenarios over the years

Hypothetical scenario analysis is an imprecise science, and industry best practices can be difficult to pin down given the qualitative nature of identifying and building scenarios. That’s why we continuously look for ways to improve our framework as we develop new MDS for the most challenging market conditions.

After developing MDS for many years and across many event types, we believe that it helps to home in on events with a clear market catalyst, and to consider a small subset of financial market variables whose significant moves could impact your client’s portfolio.

The future is anyone’s guess, but you don’t have to venture through widescale market events on your own.

BlackRock’s Market-Driven Scenarios in Aladdin Wealth™

Having our experts create the scenario analyses and push them through the Aladdin Wealth™ engine makes it easier for firms and advisors to evaluate portfolio risk with robust, forward-looking scenarios.

Our technology unifies the investment management process and provides a common data language. Advisors can personalize insights for each client’s long-term financial goals, while wealth managers can transform the business at scale.

Aladdin Wealth™ is built on the same portfolio and risk analysis technology used by BlackRock and sophisticated institutions around the world, so you can evaluate portfolios with greater transparency in any market environment.