Private equity is a core pillar of BlackRock’s alternatives platform. BlackRock’s Private Equity teams manage USD$35 billion in capital commitments across direct, primary, secondary and co-investments.

Private Equity

Why BlackRock for private equity?

Private equity is an essential element of investors’ portfolios. Investors are seeking differentiated strategies for their private equity allocations based on their unique needs, including risk and return objectives, cash flow profiles and overall cost. Our platform takes a holistic approach to investors’ private equity portfolios and is designed to offer strategies and solutions that align with client objectives and deliver persistent outperformance.

True alignment with client needs

We are built to share our advantages with clients— and steadfast in our commitment to provide efficient exposure to private equity in formats tailored to their needs.

Differentiated sourcing enabled by a centralized platform

Our sourcing machine, comprised of networks in public and private markets and a brand that has enabled proprietary access, is core to our ability to generate alpha.

Insights amplified with technology

A market-leading analytics platform provides an edge with exceptional visibility across asset classes, and deep views across companies, industries and macro trends.

Learn more about private equity at BlackRock

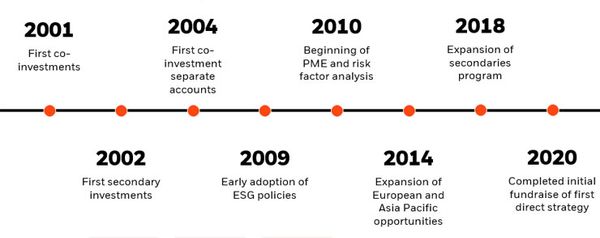

Evolution and innovation in private equity

Following two decades of strong growth, private equity now presents a large collection of strategy offerings and multiple ways to invest. BlackRock has been a major contributor to this evolution, from our role as an early mover in co-investments to our early adoption of ESG policies to our introduction of an innovative, client-aligned direct strategy.

Source: BlackRock, for illustrative purposes only.

Private equity investment strategies

Our approaches span the private equity toolkit, offering investors exposure to private equity through direct, primary, secondary, and co-investment strategies. While the approaches differ, they share the strengths of a common platform as they seek to deliver top quartile performance across investment cycles.

Direct

We are designed to deliver compounded private equity returns and better alignment with investors and investee companies. The strategy is predicated on asset selection that prioritizes proven, high-quality businesses and value creation through active collaboration with management teams.

Co-investments

We have been leaders in co-investments since 2001. More than half of co-investment capital has gone into pre-bid transactions, enabling us to do deeper due diligence, have stronger influence on results and obtain scalable allocations.

Primaries

We take a systematic approach, with long-term pipeline visibility based on comprehensive market coverage. Robust portfolio planning enables diversification across managers, vintages, strategies/stages, geographies, sectors and sizes.

Secondaries

Investors buy shares in PE funds on the secondary market to access more mature assets, diversify their portfolios and capitalize on market dislocations. Our experienced secondaries team leverages BlackRock’s advantages to deliver on all fronts.

BlackRock's latest private equity insights

On the Historical Outperformance of Private Equity

19-Nov-2024 | By Jeroen Cornel, Kyle McDermott, Yamona Win

An evaluation of private equity returns compared to their respective public market equivalents.

Systematic Insights into Private Equity Investing

11-Nov-2024 | By Systematic Investing

This research presents a framework for late-stage venture and growth equity investing, showing how quantitative tools and alternative data used in public markets may help forecast positive outcomes in growth equity investments.

Venture capital market outlook

01-Oct-2024 | By BlackRock

Explore our analysis of the venture capital market; a dynamic and rapidly evolving landscape shaped by macroeconomic shifts and technological advancements.

Mastering private equity with the BlackRock Educational Academy (BEA)

BlackRock’s private equity team help debunk common myths as it relates to drivers of performance, the use of secondaries as a portfolio management tool and also walk through case examples within primary, secondary, and co-investment examples.