In recent months, some market participants have become increasingly focused on the potential for late-cycle risks in the liquid and private credit markets – highlighting several high-profile defaults as potential warning signs. In our view, the granular fundamental data suggests these developments are more reflective of heightened dispersion, rather than widespread market disruption.

Assessing Stress Levels

Defaults are nothing new for lending in the non-investment grade space. The long-term default rate in non-investment grade loans, over multiple decades, is about 3.5%.1 Currently, we are not observing outsized evidence of defaults broadly but rather specific instances and individual losses in portfolios. With benign credit conditions for more than a decade, the average default rate has been low for an extended period of time. As a result, recent news coverage of high-profile defaults may create a false impression that the market is experiencing an inflection point of distress as opposed to a reversion to the mean.

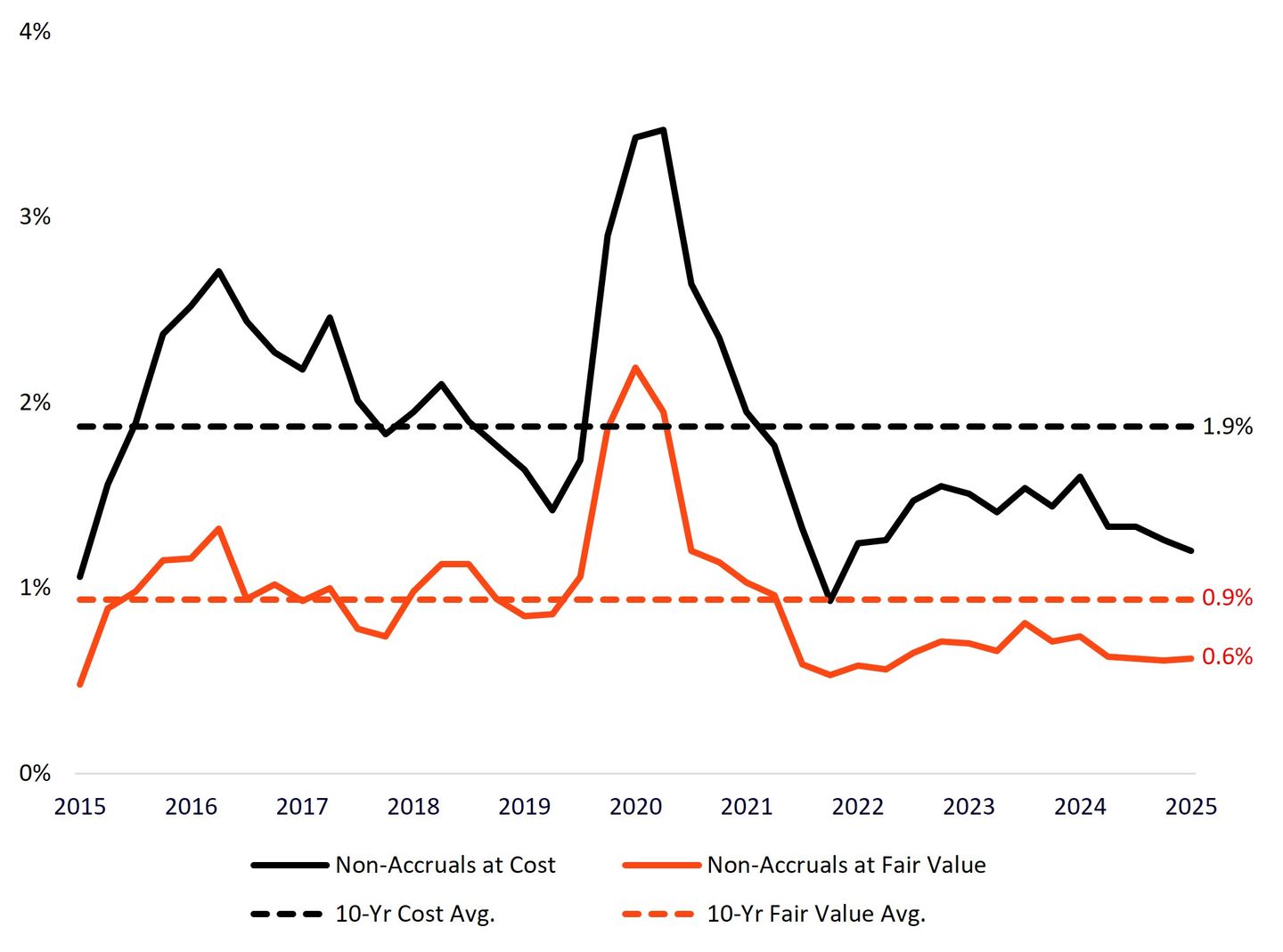

Based on Cliffwater’s data, which tracks nearly 20,000 loans across publicly traded, non-traded and private BDC portfolios, broader portfolio credit performance appears to be generally consistent with or in some cases, better than historical norms. Non-accrual rates, on both a cost and fair-value basis, remain comfortably under the respective 10-year averages and are not upward trending, suggesting credit performance has remained stable.

BDC Non-Accrual Rates2

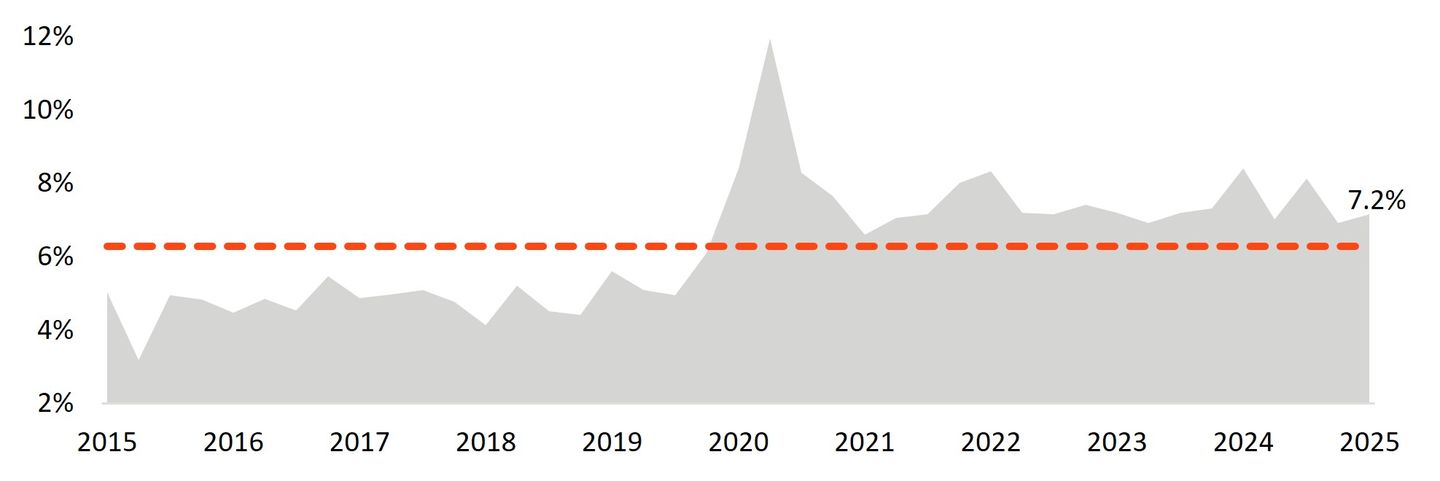

Payment-in-kind (PIK) usage, which some point to as a shadow indication of non-accruals, has increased modestly in recent quarters. However, it remains well below the elevated levels seen in 2020 and below the smaller peaks seen in each of 2022 and early 2024, indicating borrowers have not been increasing their reliance on aggressive forms of flexibility.

BDC PIK Income as Percentage of Total Income2

In our view, it’s important to delineate between ‘good’ and ‘bad’ PIK – the former use case can be a powerful tool when originating new debt that, when implemented thoughtfully, can provide benefits to both borrowers and lenders. In environments where interest rates are elevated or there is a known future catalyst for change in a company’s cash flows, structuring some degree of PIK flexibility up front can help alleviate the pressure of higher cash interest burdens on borrowers and can support a company’s ability to continue to grow. This is what we would typically classify as ‘good’ or intentional PIK.

“Bad PIK” typically refers to PIK terms put in place through an amendment based on a borrower’s request to convert some or all of its cash interest to PIK interest due to underperformance of the business. These situations vary greatly from borrower to borrower, and thoughtful evaluation of each situation is critical. Since PIK interest is added to the principal balance of the investment, it can further exacerbate a capital structure that is already over-levered. Where the underperformance is short-term in nature with a clear path to resolution, temporary PIK relief can be a useful bridging tool for borrowers, helping them avoid a default that may not ultimately be beneficial to investors.

Private Company Fundamentals in Focus

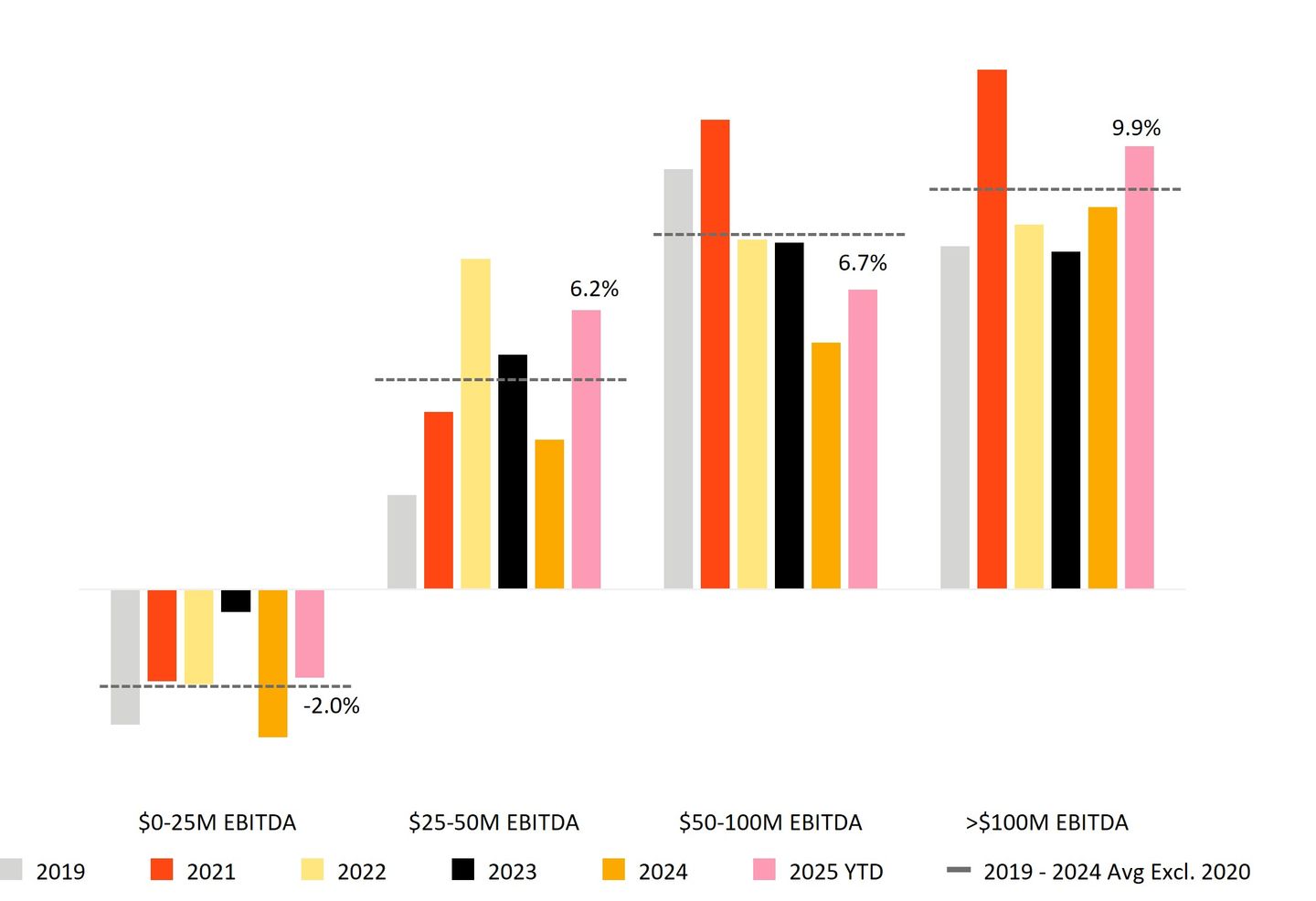

Data from Lincoln International, a prominent independent valuation agent for private credit portfolios, shows that private company fundamentals remain constructive as of the end of the third quarter. All size cohorts showed positive year-over-year trailing 12-month EBITDA growth as of September 30, 2025, except for the smallest borrowers generating less than $25 million of EBITDA.3

Growth is strongest in the upper middle market – companies with $100 million plus of EBITDA – which are posting last twelve months EBITDA growth just under 10%. As shown in the chart at the top of the next page, this is well above their average from 2019 to 2024, excluding 2020 due to the distortive impact of the COVID-19 pandemic. The core middle market – companies with $50 to $100 million of EBITDA – exhibited trailing 12-month EBITDA growth of 6.7% over the same period, demonstrating some resilience even amid a more challenging operating environment.3

Year-Over-Year Last Twelve Months EBITDA Growth Magnitude by Company Size (Based on EBITDA)3

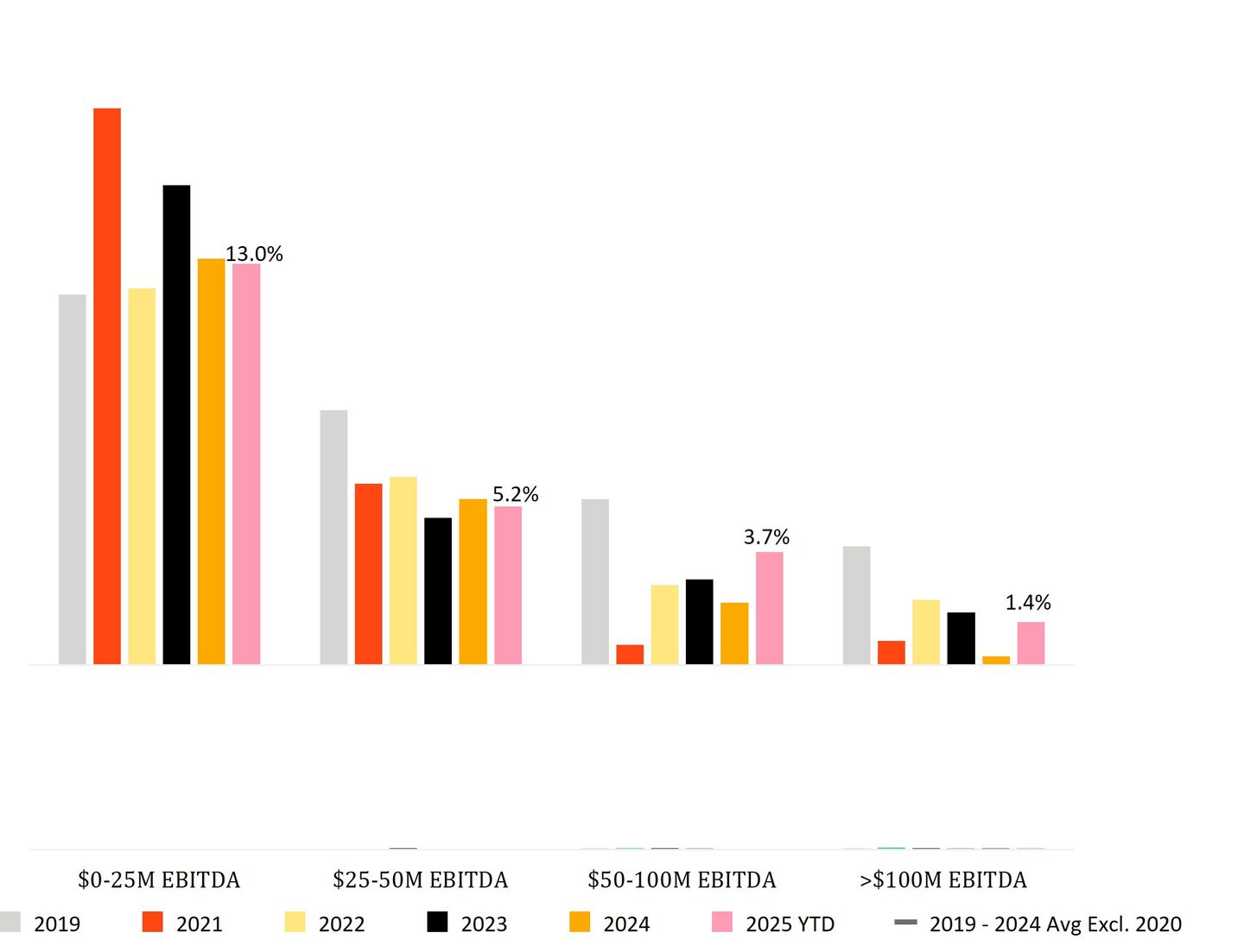

Defaults remain low at the upper end of the market, where companies with $100 million plus of EBITDA show a covenant default rate of just 1.4%, slightly under the 2019 to 2024 average excluding 2020 due to COVID-related default peaks. Defaults are higher in the core middle market but are generally in line with averages over the last five years (excluding the 2020 COVID period), indicating no broad-based stress. We see the most pressure within smaller companies, which we believe have a limited margin for error navigating macroeconomic shocks. Companies with less than $25 million of EBITDA are experiencing meaningfully higher covenant defaults, compared to companies at the upper end of the market, reinforcing our view that experienced private credit managers with scale that invest in larger companies are best positioned during challenging macroeconomic environments.

Private Company Covenant Default Rates by Company Size (Based on EBITDA)3,4

Private Credit’s Growth

The heightened concerns about the health of private credit also have led to questions about the significant growth of the asset class in recent years. In our view, the growth of private credit has been measured rather than excessive, especially when viewed alongside the expansion of private equity – the primary driver of private credit activity.

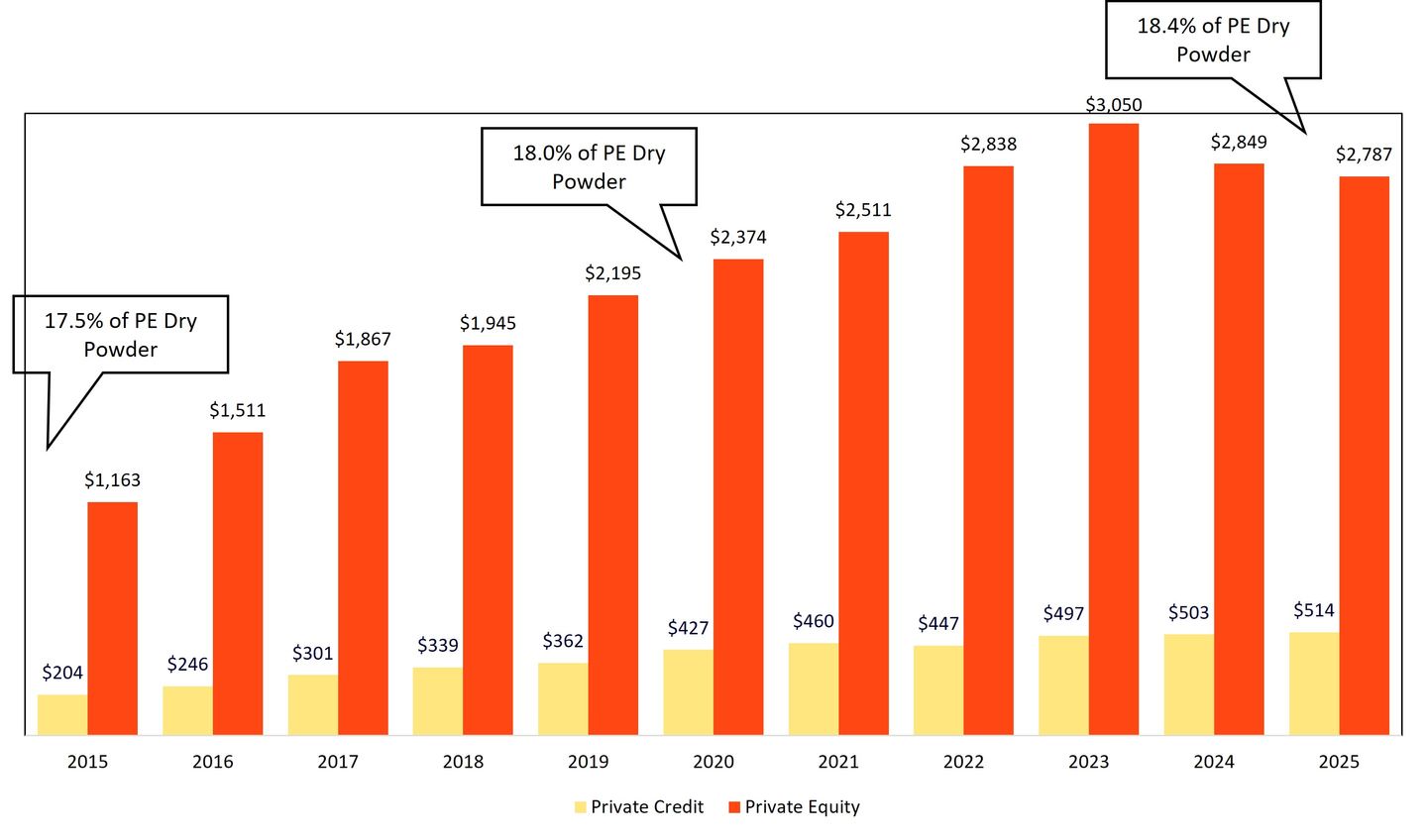

Over the past 10 years, dry powder in both private credit and private equity has grown at a similar compound annual growth rate – just over 9% – but private credit is doing so off a much lower base.5 Over the same period, private credit dry powder as a percentage of private equity dry powder has remained almost unchanged, underscoring the thesis that the market’s scale remains proportionate to its opportunity set.

Private Credit Vs. Private Equity Dry Powder ($B)5

We believe other factors are driving expansion of the addressable private credit opportunity beyond private equity as well. We have observed that companies are staying private longer, expanding the investable universe for direct lenders and supporting long-term demand for private credit solutions. We have also seen that a growing number of larger public companies are increasingly utilizing private credit financing, particularly during periods of market volatility. This has opened a new market opportunity for larger scale providers and, in our opinion, represents one of the largest potential growth vectors for the industry.

Relative Value Proposition

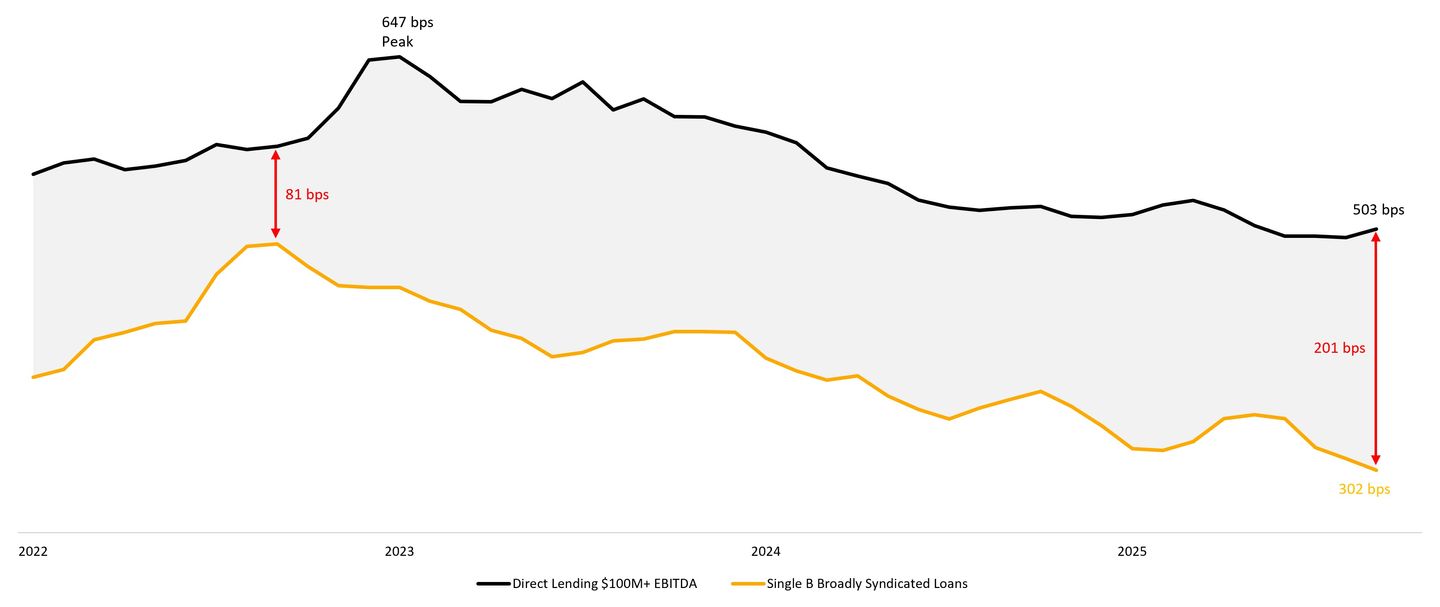

While interest rates have moved lower – with the Federal Reserve cutting five times since September 2024 – and direct lending spreads have compressed from the elevated levels of late 2023, we continue to view all-in private credit returns as attractive. We believe that it is appropriate to evaluate private credit on a relative-value basis, not in isolation. Today, direct lending is offering more than 200 basis points of excess spread return relative to new-issue single-B broadly syndicated loans, the closest comparable public-market floating rate asset class.6 This relative return potential sits at the wider end of the range dating back to 2022, underscoring that relative value remains favorable even as rates and spreads normalize. In short, despite falling base rates and tighter spreads, we feel that the premium investors receive for private credit exposure has remained robust.

Direct Lending Spreads6 Vs. Broadly Syndicated Loan Spreads7 (bps)

Conclusion

In our view, we are returning to a credit environment of normalcy following an extended period of subdued defaults. We believe private credit managers that build diversified portfolios with a focus on larger companies are best positioned to mitigate risk.

We remain positive on the private credit opportunity set as it continues to exhibit strong and resilient fundamentals, supporting long-term growth and stability. There is an expanding universe of potential investment opportunities within private credit, driven by increasing demand for non-bank lending solutions. The return profile of private credit remains compelling on a relative value basis, offering competitive yields compared to traditional fixed-income investments. In our view, private credit strategies have the potential to provide compelling risk-adjusted returns compared to traditional fixed income investments through diversification and reduced correlation to public markets.