Jean Boivin

Head of BlackRock Investment Institute

We've entered an era where supply constraints are the driving force of inflation rather than excess demand. This will likely bring more macro volatility and force policymakers to live with higher inflation.

We are in a new and unusual market regime, underpinned by a new macro landscape where inflation is shaped by supply constraints. Limits on supply have driven the surge in inflation over the past year: a profound change from the decades-long dominance of demand drivers. This fundamentally changes how we should think about the macro environment and the market implications. The key to understanding the muted response of central banks to inflation is not the timeframe but its cause: supply. Much of the 2021 debate overlooked this.

Economy-wide and sector-specific supply constraints are at play in the economic restart – these are pushing inflation higher, even though overall economic activity has not fully recovered. The restart gives a glimpse of how the transition to net-zero emissions will play out: it will be akin to a drawn-out restart with both economy-wide supply limits and big shifts across sectors creating supply bottlenecks. Whether or not carbon emissions are reduced, we believe climate change will increase inflation. An orderly transition to net-zero is the least inflationary path, in our view.

In addition, a rewiring of globalization and population ageing in China are reducing the supply of cheap imports from China to developed markets. This will raise costs and force further resource reallocation in those markets, making supply constraints more common. Geopolitical risks threaten to disrupt energy supply.

A world shaped by supply constraints will bring more macro volatility. Monetary policy cannot stabilize both inflation and growth: it has to choose between them. We think central banks should live with supply-driven inflation, rather than destroy demand and economic activity – provided inflation expectations remain anchored. When inflation is the result of sectoral reallocation, accommodating it yields better outcomes, as recent research (Guerrieri et al, 2021) shows. Insisting on stabilizing inflation would lead to an overtightening of monetary policy, more activity sacrificed and a slowing down of the needed sectoral reallocation.

This – together with the policy revolution that we will come back to in a follow-up publication – is why we expect the sum total of rate hikes in this cycle to be low. Central banks will take their foot off the gas by starting to remove stimulus – but they shouldn’t go further to fight inflation, in our view. We consider the risks to this view and the investment implications.

This new era of supply-driven inflation has been ushered in by the Covid-19 pandemic shutdowns and the economic restart that followed. The start of the pandemic was dominated by an economy-wide supply shock: activity was deliberately brought to a halt to curb the spread of the virus. As restrictions were lifted and the powerful restart took hold, it proved difficult to bring production back online as quickly.

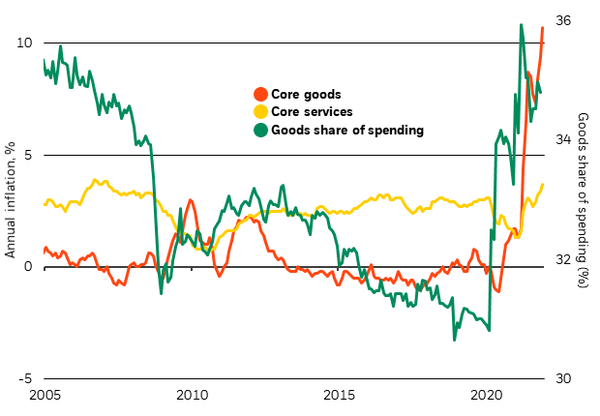

Through 2021 the restart saw the emergence of more sector-specific supply problems, driven by the sudden and sharp shift in consumer spending away from services and towards goods. This shift in the mix of demand created bottlenecks in goods-producing sectors as supply struggled to keep pace. Meanwhile, it created spare capacity in service industries. This has driven inflationary pressure in goods sectors, which have seen the largest price rises – see the chart below.

In service sectors that have lost out from the shift in spending, prices have been stickier, despite perhaps needing to fall. This is typical, but in the restart it has been reinforced by another supply constraint. Normally, sectors that are losing out tend to see lower wage growth. But due to the pandemic, people have left the labor force, particularly those that were in contact-intense services like leisure and hospitality. So, service sector companies faced with the shift in spending away from them have – unusually – been faced with rising, not falling, wage costs in their industries.

Some have attributed current high inflation to greater fiscal spending in the U.S. We see it as a contributing factor, not the primary cause. This is not a classic case of overall demand in the economy – supported by fiscal policy – being unusually high. Fiscal policy cannot explain why inflation is so high when economic activity has yet to fully recover. The fundamental constraint is that supply capacity is unusually low. This is yet another way in which this restart differs from a normal cyclical recovery. The way to deal with this inflation, in our view, is not to destroy demand, but to increase supply capacity and promote the movement of resources across sectors.

Major spending shiftU.S. goods vs. services inflation and spending, 2005-2021

Sources: BlackRock Investment Institute, U.S. Bureau of Labor Statistics, with data from Haver Analytics, January 2022. Notes: The chart shows core goods and services CPI inflation, the green line shows the share of nominal goods spending in total U.S. personal consumer spending.

We believe the economic restart provides a glimpse of what is to come. The transition to net-zero will be like a restart drawn out over decades, bringing with it new supply constraints that push up inflation – through both broad-based and sectoral channels.

The transition is fundamentally about including the costs of climate damages in economic decisions. These costs can be reflected in different ways: carbon taxes, regulations or just consumers choosing to pay more to avoid climate damages. Regardless of how the cost is internalized, we see a broad-based impact on inflation: energy costs are likely to increase, driving up producer and consumer prices. How that translates into inflation depends on the timeframe over which those increases occur. A smooth, even transition would spread out the impact. If the shift happens faster – condensing prices rises into a shorter timeframe – the impact on inflation would be more material.

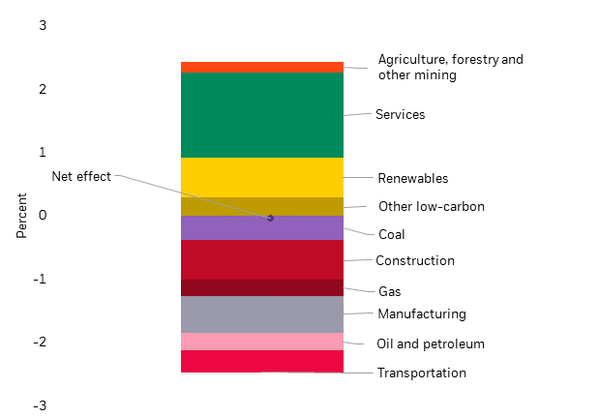

In addition, the restart shows how another often overlooked channel will operate in the transition. Supply constraints will be caused by reallocation across sectors, in this case to accommodate shifting energy demands. In their World Economic Outlook,

the IMF suggests that over 2% of global employment will ultimately need to change sector to meet these demands – see the chart. If demand shifts faster than resources are reallocated, the mismatch could push overall inflation higher – like a stretched-out version of the economic restart.

The most effective way to contain inflation during the transition, in our view, is to ensure the transition is gradual and orderly, so that supply can keep pace with shifting demand across sectors and higher energy costs can be absorbed over time. A transition left too late may keep inflation down in the short term but risks a much greater overall impact later on.

Would no transition at all be a better strategy for containing inflation? Not in our view: while the transition – even an orderly one – is likely to bring higher inflation, we believe it will still deliver a better outcome in terms of both the level and volatility of inflation than a failure to act. No climate action would mean rising global temperatures, more frequent severe weather events and greater economic damage: in previous work, we estimated that no climate action would result in a cumulative loss in economic output of nearly 25% over the next 20 years. We would expect more frequent and sharp spikes in energy, food and other prices due to severe supply constraints – akin to a pandemic on repeat.

Labor shifts needed for transitionNet employment change, 2020 vs. 2052

Sources: BlackRock Investment Institute and IMF, September 2021. Notes: The chart shows the contribution of different sectors to the global change in employment between 2020 and 2052 as a result of the green transition, in IMF simulations using the G-cubed macroeconomic model; see the IMF World Economic Outlook 2020, chapter 3.

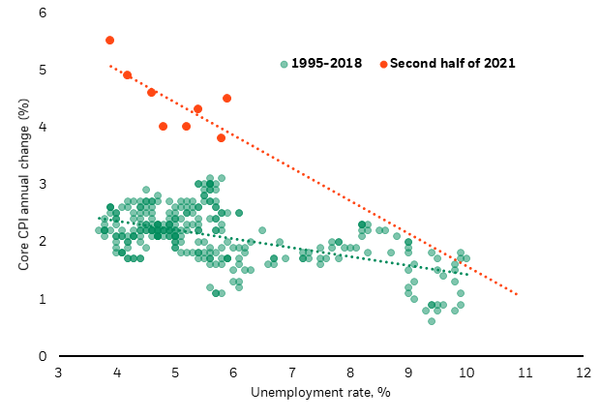

A world shaped by supply constraints will bring more macroeconomic volatility. There is no way around this because – unlike when inflation is driven by demand – policy cannot stabilize both inflation and growth at the same time: it has to choose between them. In other words, central banks have to either accept higher inflation or destroy demand to squeeze wages and prices to rein in inflation. Given the historical relationship between unemployment and inflation, if central banks had sought to keep inflation close to 2% amid the supply constraints experienced in the restart, this would likely have meant needing to drive the unemployment rate up to nearly double digits – see the chart.

Greater macro volatility – in both growth and inflation – implies greater market volatility and higher risk premiums on both bonds and equities. To minimize growth volatility, central banks will want to live with supply-driven inflation, provided inflation expectations do not become unanchored. This is one reason why the current policy response to higher inflation has been much more muted than in past episodes – a key theme in our 2022 Outlook. Recent research (Guerrieri et al, 2021)

says that central banks should accommodate inflation if caused by a need to reallocate across sectors. Doing so allows prices to rise in sectors benefiting from greater demand, relative to prices in sectors losing out. This helps economies to adjust and ultimately means supply constraints are less persistent.

We think central banks should live with current inflation pressures for now. They will likely take their foot off the gas this year by removing stimulus and returning rates toward more neutral settings – but this is a far cry from slamming on the policy brakes to deliberately destroy activity and bring inflation down. Notably, despite bringing forward materially the expected path of Fed rate hikes in recent weeks, markets are still pricing a muted overall hiking cycle.

Yet we expect negative bond returns this year. This has less to do with central bank policy than it does with the intrinsic features of this macro landscape. Faced with more inflation volatility, investors would question – as they have in recent weeks – the perceived safety of holding longer-term government bonds at historically low yield levels. Higher yields from a renewed term premium – which has largely been near or below zero in recent years – are not ultimately bad for stocks if they reflect a relative shift of investor preferences away from bonds and towards other assets. In fact, a muted central bank response to inflation means we expect inflation to persist without damage to growth, supporting risk assets in the longer term. This is why we are underweight government bonds on both a tactical and strategic horizon.

The primary risk we see is that central banks hit the brakes if constraints persist and they perceive that higher inflation could feed into inflation expectations. This would be bad for bonds and stocks as policy rates rise to restrictive levels and slow growth. Some of that risk may be priced in at points – like in recent weeks – as markets adapt to this new macro landscape. But if central banks do hit the brakes, they will likely learn that it comes at too great a cost and will be forced to reverse course. At the points this risk is priced, yield curves will tend to flatten or even invert.

High cost of pushing inflation downU.S. unemployment rate and CPI inflation, 1995-2021

Source: BlackRock Investment Institute, U.S. Bureau of Labor Statistics, with data from Haver Analytics, January 2022. Notes: The chart shows the U.S. unemployment rate (horizontal axis) compared with the U.S. annual core inflation rate (measured by the year-on-year percentage change) for different periods (vertical axis). All data are at monthly frequency.

Read our past macro and market perspectives research >here.

As a global investment manager and fiduciary to our clients, our purpose at BlackRock is to help everyone experience financial well-being. Since 1999, we've been a leading provider of financial technology, and our clients turn to us for the solutions they need when planning for their most important goals.