April 17, 2026 | By Emma Chu

Key points

01.

AI could reshape earnings, but unevenly

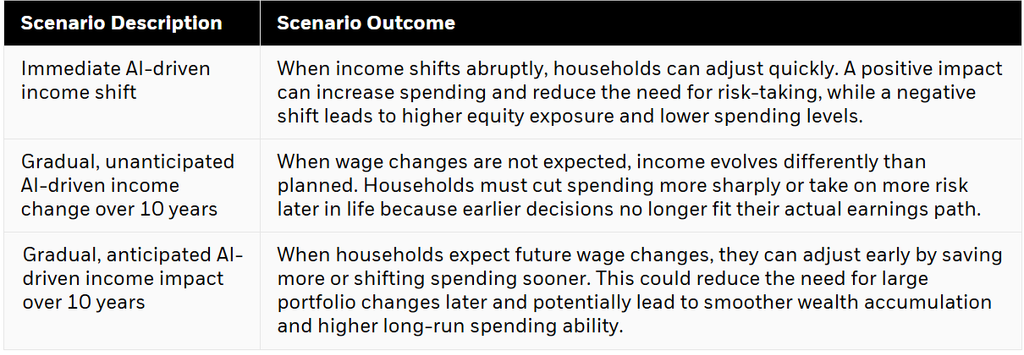

Income paths across occupations could disperse and widen, making earnings less predictable and compounding financial planning risk.

02.

Anticipation can improve outcomes

When workers can anticipate potential earning shifts, they may be able to make earlier adjustments and achieve smoother outcomes.

03.

Longer lives can increase retirement strain

AI could help lengthen lives, which could require savers to make modest early-retirement spending cuts and consider more stable-income strategies.

Artificial intelligence (AI) is rapidly transforming industries, altering how people work—and earn their paychecks. It’s also impacting life expectancy, with medical advancements that are aiming to improve research and healthcare. As these trajectories evolve, the implications for retirement planning are significant. Advisors will play a critical role in helping clients navigate the shifting income patterns and potentially longer lives that may impact their ability to afford a more financially secure retirement.

To evaluate these changes, we modeled how AI-driven shifts in wages and life expectancy could influence saving behaviors, investment decisions, and long-term retirement spending ability. This research integrates lifecycle modeling with empirical analysis of AI exposure across job tasks, offering a forward-looking perspective on how financial planning must adapt to this new era.

Understanding & preparing for a new earnings landscape

This research suggests that AI is likely to affect wages across most occupations, but not evenly. By looking at how tasks within jobs have changed in the past—and using AI to estimate how current tasks may evolve—the study finds a wide range of potential wage outcomes across occupations. Some roles may benefit from productivity gains and new tasks, while others may face pressure from automation or reduced labor demand.

Occupations appear to be exposed to AI in two areas: repeated tasks and technological tasks. Our findings, shown in the chart above, are as follows:

- Full Automation (Automated). Occupations with repeated, non-technological tasks are most likely to have their tasks automated (e.g. low-skilled functions that can be substituted by capital, either in software or hardware).

- More with More (Complemented – Increase Output). Occupations with idiosyncratic, technological tasks are most likely to be enhanced by AI without adverse impacts on labor market demand; these professions require creative decision-making or drive cutting-edge research (e.g. medical innovation, specialized repair technicians).

- More with Less (Complemented – Reduce Labor). Occupations with repeated, technological tasks are likely more susceptible to AI improving labor productivity while shrinking aggregate labor demand; examples include areas where large language models can significantly scale the output of a small number of workers (e.g. computer programming, administrative, and legal tasks).

- No Automation (Unaffected). Occupations with idiosyncratic, non- technological tasks are least likely to be affected by AI; tasks that require in-person or inter-personal relationships, action, and specialization may be relatively insulated from AI (e.g. nursing.)

Importantly, this work is still at an early stage: AI adoption is evolving quickly, and the full economic impact is not yet known. The goal is not to predict exact winners and losers, but to highlight that income paths may diverge meaningfully.

Why does this matter for retirement? Consistent saving during working years is the critical driver of retirement readiness, and so understanding and preparing for AI’s potential and uneven impact across occupations can help ensure people stay on track despite a changing labor market.

During a person’s working years, labor income is their primary fuel for savings. Even small, persistent changes in wages—positive or negative—can compound over decades into very different retirement outcomes. If AI dampens wage growth in certain occupations, savings capacity may decline; if it boosts productivity and that flows into wages, savings potential improves. Just as with other potential shocks, the key insight is that anticipating these shifts early allows:

- Individuals to adjust their savings rates

- Employers to refine plan design

- Policymakers to consider supportive measures

Our lifecycle model incorporates assumptions about income, mortality and market returns, drawing on foundational data from the Panel Study of Income Dynamics (PSID), the Current Population Survey (CPS) and mortality tables from the Society of Actuaries. These datasets are central to our evolving Retirement Solutions toolkit and provide a foundation for simulating optimal savings and equity allocations under normal economic conditions.

We introduce the impact of AI into the model as an externally driven income shift, either positive or negative, and as a factor that may reshape earnings trajectories across occupations. Our broader empirical research shows that AI widens the dispersion of potential income paths, even when average income growth remains steady. The core planning challenge is that income becomes less predictable, and the effects of that unpredictability can compound over time.

The model illustrates these effects through three scenarios that highlight how timing and anticipation shape outcomes.

AI-driven longevity is rewriting retirement

AI’s influence extends beyond labor markets. Advances in healthcare, diagnostics and personalized treatments may increase life expectancy. To assess the financial implications, we modeled higher average lifespans without changing overall age-based mortality patterns.

As lifespans lengthen, our modeling illustrates that individuals can support spending for a greater number of retirement years through a modest reduction in spending in early retirement years. This is shown in the top chart below. As shown in the bottom chart, equity allocations also moderate slightly as households look to plan for more consistent spending over an extended horizon, although maintaining appropriate risk-taking remains essential. Longer lives mean longer drawdown periods, increasing exposure to market volatility, sequence risk and inflation, which raises the importance of strategies that can support stable income over time.

Modelled impact of changes in life expectancy on retirement spending and portfolio allocations

Source:

Average consumption for different shocks to life expectancy. Source: BlackRock. As of August 2025.

Source:

Average equity allocation for different shocks to life expectancy. Source: BlackRock. As of August 2025.

Source: BlackRock. For illustrative purposes only. The income, consumption rates and wealth values shown are hypothetical estimates generated using Monte Carlo simulation, which is a statistical modeling technique that forecasts a set of potential future outcomes based on the variability or randomness associated with historical occurrences. Projections are hypothetical in nature, do not reflect actual investment results and are not guarantees of future results. No representation is made that an investor will achieve results similar to those shown. Actual values could be higher or lower based upon a number of factors and circumstances not addressed herein.

Building resilience for a longer, less predictable future

Together, the AI labor and longevity shocks applied in our analysis highlight that AI increases the range of possible financial futures, not necessarily their average trajectory. This creates a clear imperative to help clients navigate greater uncertainty with more adaptive planning tools.

Our research identifies several strategies that can help individuals mitigate the financial effects of income volatility and longer lifespans.

- Anticipation and dynamic planning - Planning ahead is the most powerful mitigant. When households factor potential income dispersion into their financial decisions – saving slightly more and maintaining thoughtful equity exposure – they may achieve smoother outcomes even when disruptions may occur. Anticipation expands financial flexibility and reduces the need for significant later-life adjustments.

- The role of alpha over longer horizons - In a world where people live longer and disruptions may occur, even modest amounts of consistent alpha can compound more meaningfully. Persistent excess return in the range of 0.3% to 0.5% can materially offset the added costs of longer retirements. LifePath® Dynamic target date funds are designed to capture these benefits by incorporating active insights into the glidepath and seeking opportunities for excess return throughout the retirement horizon. As markets evolve alongside AI, active management may uncover new opportunities, which can further support long-term outcomes.

- Reliable income strategies and plan design – Retirement Income solutions, such as BlackRock’s LifePath Paycheck® or decumulation-oriented strategies, can help hedge longevity risk. By reducing uncertainty around essential expenses, these tools can support more stable spending patterns throughout retirement, especially when life expectancy is rising. Plan sponsors can incorporate these options within flexible plan designs that reflect both labor income variability and changing needs for retirement spending.

Preparing clients and their portfolios

AI is introducing new forms of uncertainty across both labor markets and healthcare. For retirement planning, the growing variability in lifetime income and longevity is a core challenge. These forces make anticipation, flexibility, and resilience more important than ever.

The BlackRock Retirement Solutions team, armed with our lifecycle strategies, active capabilities, income solutions, and analytic tools, is uniquely positioned to help advisors and plan sponsors navigate this evolving environment. By integrating forward-looking planning, disciplined risk management, and reliable income strategies, clients can build confidence in their long-term financial futures, even as technology continues to change how we work, invest and retire.

LifePath® target date strategies

Our target date approaches aim to address one retirement challenge: improving participant outcomes with great certainty and consistency.