Salary proxies and contribution rate (median 10%) derived from survey participant data. Assumptions include retirement age 65 and starting age 25 and do not include company stock or DB to salary ratio (pension income replacement).

2026 Read on Retirement®: A new era of retirement

Participants and plan sponsors are optimistic about retirement, yet BlackRock's Read on Retirement® reveals a gap between retirement expectations and projected outcomes. The report explores the new capabilities participants and sponsors are embracing to help close that gap, from active management and private markets to guaranteed income

Key takeaways

01.

Confidence is rising, preparedness is still catching up

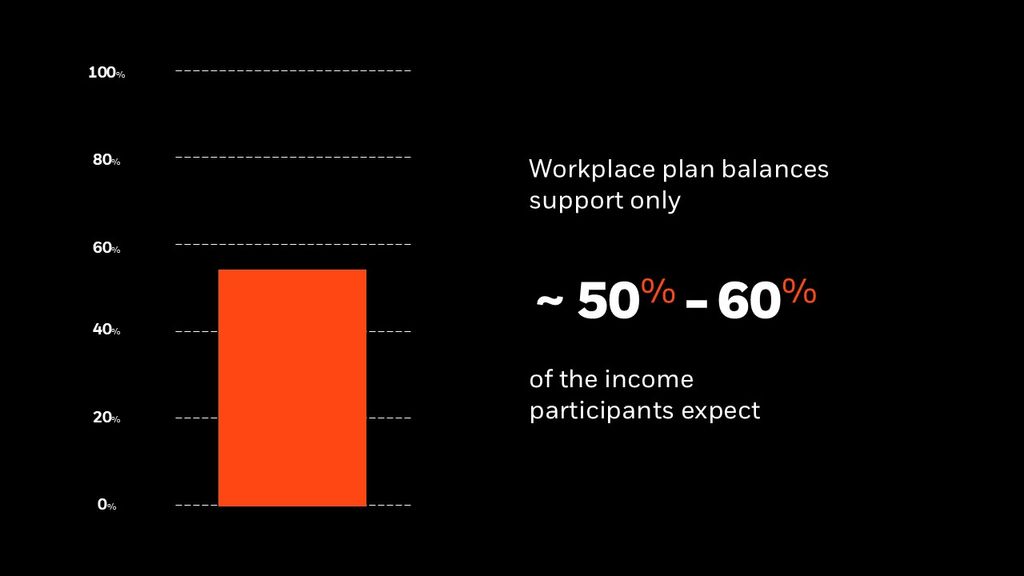

68% of savers feel on track, yet projected balances cover only 50–60% of the retirement income they expect . The challenge is capacity: savers recognize the gap, but competing financial priorities make it harder to close.

02.

New capabilities to turn optimism into reality

Participants are increasingly embracing capabilities designed to improve retirement outcomes beyond traditional savings strategies, including active management, private markets, and guaranteed income.

03.

Technology and AI are accelerating engagement

81% of savers want tailored guidance and emerging technologies are creating an opportunity to make targeted education more accessible for sponsors, with 1 in 4 are already using AI-generated guidance.

Confidence and preparedness are not always the same thing

Savers and sponsors feel optimistic about retirement

68% of participants say they are on track and 66% of employers agree. It's possible that stronger markets and investment performance are contributing to some of that optimism.

Looking beyond sentiment at savings behavior

Our analysis shows savers are only on track to replace about 50 –60% of the retirement income they expect their workplace savings to provide.

Americans understand they need to save more

Participants say they need to contribute 15% of pay but contribute only 10% today, and over half may need to reduce contributions as financial pressures mount.

Closing the readiness gap with new capabilities

Participants are responding by looking to new capabilities and sponsors are expanding their retirement toolkits.

Capacity challenges vary across life stages

Many savers face practical barriers to closing the gap, and each generation experiences retirement challenges differently and differently than generations past.

Retirement window generation

Health risks and longevity concerns

Experiencing the years in and around retirement when outcomes are fragile. The first generation largely retiring without a pension.

Sandwich generation

Supporting family while saving

More likely to reduce contributions while balancing growing retirement balances and competing financial priorities.

Most runway generation

Debt and income concerns reshape saving behavior

More likely to reduce retirement savings due to debt and lower confidence in future income, while placing greater emphasis on long-term investing and exploring options.

The next frontier: 'Personal Pensions'

Participants and sponsors are converging around the capabilities that made pensions powerful: professional management, diversified investing, and retirement income. Today, workplace plans increasingly have the opportunity to deliver those same capabilities through active management, private markets, and guaranteed income.

55%

of savers with a preference prefer active target date funds over index

45%

of sponsors are considering adding private market exposures

88%

of savers want secure income options in their workplace plan

Technology and AI are accelerating engagement

Participants are asking for more personalized support—from tools that show whether they're on track to tailored education and guidance. Technology and AI are accelerating the way sponsors engage more effectively and at greater scale.

81% of savers want tailored guidance

41% are already going to LLMs for their financial question

1 in 4 sponsors are already using AI-generated guidance

Download the PDF

ADDITIONAL RESOURCES

Inside retirement

Stay informed with the latest retirement insights, research and thought leadership.