Key points

01.

A buffer can help keep retirement savings on track

02.

Tools empower saving habits

03.

Timing is key

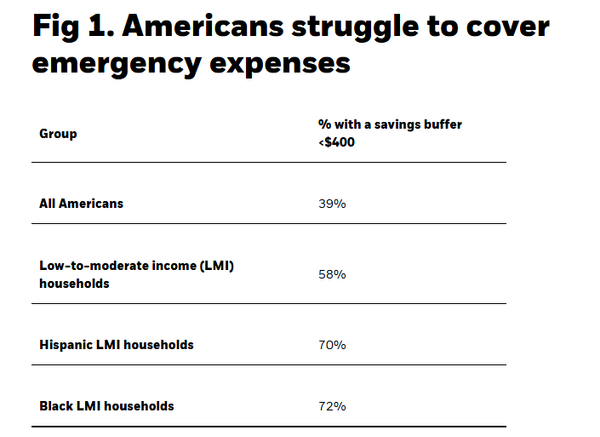

The $400 eye-opener

With the passage of SECURE 2.0, in-plan emergency savings solutions are now another tool in plan sponsors’ kits. What have the past five years of research taught us about the connection between short-term and long-term financial security? And how can 401(k) plans benefit from lessons learned?

It was the shot heard round the financial security world. In 2017, a Federal Reserve report found that four in 10 Americans couldn’t cover an unexpected $400 expense.1 (Fig. 1) In the years that followed, several organizations – including BlackRock’s Emergency Savings Initiative – mobilized to identify the tools and opportunities people need to be able to set aside money for the future.

Federal Reserve, Report on the Economic Well-Being of U.S. Households in 2017, 2018 and Commonwealth, Addressing Inequity.

Better buffers

Today, it’s widely acknowledged that having a liquid savings buffer can help individuals stay on track for longer-term retirement saving. After all, it’s hard to save for tomorrow if you’re worried about making ends meet today. The pandemic made that especially clear, and it’s something policymakers are taking seriously, as evidenced by the inclusion of the Emergency Savings Act of 2022 in SECURE 2.0 – which allows for in-plan emergency savings programs, as well as an employer match on workers’ emergency savings contributions.

With the availability of new in-plan emergency savings solutions, we wanted to know:

- Just how big a buffer is needed to insulate long-term retirement savings from short-term spending needs?

- What is the risk that emergency savings “cannibalize” retirement plan contributions?

- What best practices from emergency savings studies can be applied to retirement savings?

For more insight into what we found out about the correlation between short-term and long-term savings, download the paper below to read on.

Download the paper

How to optimize retirement income

BlackRock worked with the Bipartisan Policy Center to lift the veil on how to optimize retirement income – and the role policymakers have to play in advancing financial security.

The five forces shaping U.S. retirement

Our report identifies five trends that are shaping retirement and points to areas where we can convert challenges into opportunity - so that every American can enjoy the secure retirement they deserve.