Leveraging MSCI ESG Ratings and research coverage, MSCI ESG Research creates ESG ratings and metrics for approximately 69,000 multi-asset class mutual funds and ETFs globally. MSCI ESG Fund Ratings aim to provide fund-level transparency to help clients better understand and measure the environmental, social and governance (ESG) characteristics of a portfolio, and rank or screen funds based on a diverse set of ESG exposure categories.

SUSTAINABILITY CHARACTERISTICS FAQ

We are committed to providing investors with transparency in order to enable them to make informed investment decisions. A growing number of investors are interested in understanding the sustainability profiles of their investments and we strive to provide our clients access to this information.

MSCI ESG Fund Ratings

To be included in standard universe a fund must pass the following four criteria:

- For funds with a fund asset class other than bond or money market, at least 65% of the fund’s gross weight must come from covered securities. For funds with a fund asset class of bond or money market, at least 50% of the fund’s gross weight must come from covered securities. The ESG Fund Ratings methodology imposes a lower coverage threshold on bond and money market funds because they generally have higher exposure to asset classes that are currently out of scope for ESG analysis, including asset backed securities, mortgage-backed securities, and municipal bonds. The coverage criterion does not apply to funds that are part of the underlying holdings of another fund.

- Cash positions and other asset types not relevant for ESG analysis are removed prior to calculating a fund’s gross weight.

- The absolute values of short positions are included in a fund’s gross weight calculation but are treated as uncovered for ESG data purposes.

- The security asset type must allow recourse to the rated issuer.

- The fund holdings date (the latest date that fund reported its holdings) must be less than 1 year old.

- The fund must have at least 10 securities (this criterion does not apply to funds of funds).

- The fund must not be in the commodity asset class.

Fund ESG Ratings and other fund-level metrics are still calculated for funds that fail to meet the 65% coverage criterion but pass the other criteria However, ESG Fund Ratings reports are not issued for such funds, nor are these funds included in MSCI ESG Fund Ratings and Climate Search Tool. These funds do not impact the percentile calculations for other funds and the values for the Fund ESG Quality Score – Global Percentile and Fund ESG Quality Score – Peer Percentile metrics are not calculated for such funds. As with any fund, fund metrics will only be based on covered holdings.

The MSCI ESG Fund Ratings is designed to assess the resilience of a fund’s aggregate holdings to long term ESG risks. Highly rated funds consist of issuers with leading or improving management of key ESG risks. Each fund in the coverage universe will receive an overall “Fund ESG Quality Score” (0-10) as well as an Environmental, Social and Governance Score (0-10). The overall “Fund ESG Quality Score” aggregates issuer-level ESG scores to provide investors with an indication of the overall fund-level ESG score based on the fund’s underlying holdings. The Fund ESG Rating is calculated as a direct mapping of the 0-10 Fund ESG Quality Score to the letter rating categories of the Fund ESG Rating. The 0 to 10 scale is divided into seven equal parts, each corresponding to a Fund ESG Rating letter rating. Every possible Fund ESG Quality Score falls within the range of only one letter rating.

Percent by weight of a fund's holdings that have ESG Data.

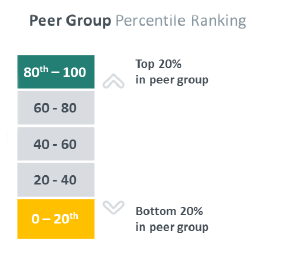

The Fund ESG Quality Score – Peer Percentile metric (1-100) represents the percentage of funds in a fund’s peer group with an ESG Quality Score equal to, or lower than, the fund’s ESG Quality Score. The peer groups are defined using the Lipper Global Classification Scheme.

The following criteria must be met for a fund to receive a Fund ESG Quality Score – Peer Percentile assessment:

- The fund must be categorized by the Lipper Global Classification scheme.

- The peer group must contain at least 30 funds.

- The standard deviation of the Fund ESG Quality Score within the peer group must be greater than, or equal to, 0.1

For illustrative purposes only. This example does not represent the results of a specific investment product.

Funds within one Lipper Global Classification (LGC) sector invest in the same financial markets or specific segments of those markets but may adopt different investment strategies or styles to achieve their investment objectives. As a general rule a fund must hold a prevalent exposure with a threshold set at 75% of its portfolio in order to meet an LGC requirement. Since temporary changes in strategic asset allocation with divergences from the historical pattern may be possible, it is essential to look at historical data to meet the specific classification requirement.

The number of holdings used to calculate the Fund ESG Score - Peer Percentile. This is based on the Lipper Global Classification and reflect the funds that are in the MSCI ESG Fund Metrics coverage universe.

Calculating the Fund ESG Quality Score requires calculating the Weighted Average ESG Score as an intermediate step. Fund holding weights are typically available based on the total fund value, but the weights used to calculate the Weighted Average ESG Score need to be adjusted for differences in ESG coverage as follows:

- Start with holding weights disclosed by the fund (wd).

- Recalculate holding weights after removing all short positions (ws).

- Remove all securities that do not have an Overall ESG Score (wc).

- Rebase the remaining weights to add up to 100% (wr).

The Fund Weighted Average ESG Score is calculated as the weighted average of Overall ESG Scores of a fund’s underlying holdings using the rebased weights mentioned above.

𝐹𝑢𝑛𝑑 𝑊𝑒𝑖𝑔ℎ𝑡𝑒𝑑 𝐴𝑣𝑒𝑟𝑎𝑔𝑒 𝐸𝑆𝐺 𝑆𝑐𝑜𝑟𝑒 = ∑(𝐸𝑆𝐺𝑖 ) × 𝑛 𝑖=1 (𝑤𝑖,𝑟)

Where:

- 𝐹𝑢𝑛𝑑 𝑊𝑒𝑖𝑔ℎ𝑡𝑒𝑑 𝐴𝑣𝑒𝑟𝑎𝑔𝑒 𝐸𝑆𝐺 𝑆𝑐𝑜𝑟𝑒 is the Fund Weighted Average ESG Score.

- ESGi is the Overall ESG Score of holding i.

- wi,r is the rebased weight of holding i.

The Overall ESG Score of a security held by a fund is assessed by taking either the Final Industry-Adjusted Company Score (for a company) or the Government Adjusted ESG Score (for a country) of the issuer. The methodologies used to determine issuer level scores for companies and countries are described in “ESG Ratings Methodology” and “ESG Government Ratings Methodology,” respectively.

The Fund ESG Quality Score is equal to the Fund Weighted Average ESG Score.

For illustrative purposes only. This example does not represent the results of a specific investment product.

The range, and average, of Fund ESG Quality Scores varies widely across peer groups. Many factors, such as regional concentrations, can contribute to peer group differentiation. While a particular peer group may tend to have high, or low, Fund ESG Quality Scores, the peer group percentiles signal how each fund ranks within its group.

MSCI Weighted Average Carbon Intensity

The Weighted Average Scope 1+2 Carbon Intensity (tCO2e/$M sales) measures a fund's exposure to carbon intensive companies. The figure is the sum of security weight (normalized) multiplied by the security Scope 1+2 Carbon Intensity.

For illustrative purposes only. This example does not represent the results of a specific investment product.

The percentage of a portfolio's market value with Carbon Intensity data.

MSCI Implied Temperature Rise (ITR)

The ITR metric is used to provide an indication of alignment to the temperature goal of the Paris Agreement for a company or a portfolio. ITR employs open source 1.55° C decarbonization pathways derived from the Network of Central Banks and Supervisors for Greening the Financial System (NGFS). These pathways can be regional and sector specific and set a net zero target of 2050, in line with GFANZ (Glasgow Financial Alliance for Net Zero) industry standards. We make use of this feature for all GHG scopes. This enhanced ITR model was implemented by MSCI on February 19, 2024.

The ITR metric is calculated by looking at the current emissions intensity of companies within the fund's portfolio as well as the potential for those companies to reduce its emissions over time. If emissions in the global economy followed the same trend as the emissions of companies within the fund's portfolio, global temperatures would ultimately rise within this band.

Note, only corporate issuers are covered within the calculation. A summary explanation of MSCI’s methodology and assumptions for its ITR metric can be found here.

Because the ITR metric is calculated in part by considering the potential for a company within the fund’s portfolio to reduce its emissions over time, it is forward-looking and prone to limitations. As a result, BlackRock publishes MSCI’s ITR metric for its funds in temperature range bands. The bands help to underscore the underlying uncertainty in the calculations and the variability of the metric.

For illustrative purposes only. This example does not represent the results of a specific investment product.

This forward-looking metric is calculated based on a model, which is dependent upon multiple assumptions. Also, there are limitations with the data inputs to the model. Importantly, an ITR metric may vary meaningfully across data providers for a variety of reasons due to methodological choices (e.g., differences in time horizons, the scope(s) of emissions included and portfolio aggregation calculations).

- There is not a universally accepted way to calculate an ITR.

- There is not a universally agreed upon set of inputs for the calculation.

- At present, availability of input data varies across asset classes and markets. To the extent that data becomes more readily available and more accurate over time, we expect that ITR metric methodologies will evolve and may result in different outputs. Funds may change bands as methodologies evolve.

- Where data is not available, and / or if data changes, the estimation methods vary, particularly those related to a company’s future emissions.

The ITR metric estimates a fund’s alignment with the Paris Agreement temperature goal based on a credibility assessment of stated decarbonization targets. However, there is no guarantee that these estimates will be reached. The ITR metric is not a real time estimate and may change over time, therefore it is prone to variance and may not always reflect a current estimate.

The ITR metric is not an indication or estimate of a fund’s performance or risk. Investors should not rely on this metric when making an investment decision and instead should refer to a fund’s prospectus and governing documents. This estimate and the associated information is not intended as a recommendation to invest in any fund, nor is it intended to indicate any correlation between a fund’s ITR metric and its future investment performance.

Want to learn more about sustainable investing?

Want to learn more about sustainable investing?

Information about MSCI ESG Fund Ratings and is sourced from MSCI. For more information please visit the MSCI ESG Fund Ratings methodology and MSCI ITR methodology.