Explore the world of private markets - a market where investors trade assets like private equity, private credit, infrastructure, and real estate privately, rather than on public stock exchanges. Your hub of private markets fundamentals. All you need to know about investing in private markets.

Discovering private markets

Capital at risk. The value of investments and the income from them can fall as well as rise and are not guaranteed. Investor may not get back the amount originally invested.

Private Markets

As an individual investor, navigating the world of private markets can seem complex. Let’s demystify the jargon, clarify the complexities, and provide you with valuable insights into this crucial aspect of the investment landscape.

The basics to private markets investing

Private markets involve trading in securities, assets, and investment opportunities that aren't available on the public market/stock exchange like the London stock exchange. Compared to the public market, private markets are larger, are growing quickly1, and play a significant role in the global economy, opening doors to potential new sources of return. Although they have a significant impact, private markets are often less familiar than public ones and carry their own unique risks.

Types of private markets' investment you can invest in

Why investors are interested in private markets

Many private market investments are deeply integrated into our daily lives—such as roads, energy grids, and technology. They have the potential to offer returns even during economic downturns, presenting an alternative to more traditional investment strategies.

Potential diversification

Investing in private markets means putting your money into things that aren’t easily bought and sold on public stock exchanges, making them less liquid than other asset classes. These investments often have risks that don’t move in the same direction as regular stocks or bonds you can buy publicly. This means they can help spread out the risk in your investment portfolio so, adding private markets investments could mitigate the overall risk your investment is exposed to.

Risk: Diversification and asset allocation may not fully protect you from market risk.

Inflation mitigation

Private markets investments involves investing in things that hold their value even when prices of goods and services go up, which can be a typical feature of real assets. Real assets tend to increase in value over time, keeping pace with, or even outpacing inflation. For example, imagine a toll road. When inflation goes up, the cost of maintain the roads increases and so the tolls people pay to use the road also increases. The rising price increases the road’s income alongside inflation, covering the cost of maintain the road and helping to protect against the effects of inflation.

It’s important to note that rising prices/higher inflation can worry investors and impact their confidence in the stock market, which can have an effect on share prices of public markets’ assets.

Seeks higher stable income

Private markets investments have the potential to deliver higher long-term stable cash throughout a varied market cycle.

For example, public bonds are issued from the government or companies when they need capital, and investors buy these bonds in exchange for fixed returns in the form of fixed interest payments. Whereas private credit investing leverages a wide range of strategies throughout market cycles, that aren’t available in public markets, and therefore could lead to investors potentially achieving higher returns compared to liquid public bonds. A popular strategy in private credit – direct lending, typically has low default rates. This is largely due to loan structuring, where private lenders can put in place mechanisms around the company’s assets for example, to ensure investors are protected as much as possible from default risk. Loans may be structured as floating rates which provide some protection against rising rates – as interest rates increase the interest the business pays increases accordingly. The interest can provide a reliable income stream. Other strategies could be opportunistic credit – often deemed as mispriced investments where investors aim to generate higher returns, or distressed lending – where investors can target credit to companies that are impacted by special events.

Enhanced potential returns

In return for investing in less liquid assets like private markets’ assets, investors can expect higher potential returns compared to public markets, called an ‘illiquidity premium’ or a ‘return premium’, as there is a higher risk the investment may fall through. This compensation could be higher levels of income from illiquid infrastructure holdings, or greater capital gains from private equity.

The key to a well-rounded investment portfolio

It’s important to consider a healthy dynamic mix of both private and public markets to ensure your portfolio is set up for the long-term. Let’s see the main differences between public and private markets assets.

Private markets more accessible to all investors

Historically private markets’ investments have only been available to institutional investors. Thanks to recent regulatory changes2, it’s becoming easier for all investors to access private market assets.

Europe’s investment vehicle of choice, the European Long-Term Investment Fund (ELTIF), has flexible features like lower investment minimums and liquidity options, allowing new individual investors the opportunity to take advantage of their potential benefits.

Similarly, the UK can also utilise another regulated vehicle: Long-Term Asset Fund (LTAF). The LTAF is designed to overcome the historical challenges of implementing alternatives in UK investment portfolios.

Understanding returns and fees

Let’s break down the mechanics around the different fees and how investors receive potential returns.

Returns

Returns are derived differently from private equity and private debt strategies. Private equity investing, including infrastructure and real estate equity, aim to generate returns through capital appreciation and income generation.

- Capital appreciation occurs when the value of the invested companies increases over time. This can happen through operational improvements, strategic changes, or industry growth.

- Income generation comes from dividends or distributions paid out by the invested companies.

Investors may start to see returns either through dividends or distributions as the companies within the fund mature or are sold.

Private credit investing, including infrastructure and real estate debt, aim to generate returns through interest payments and principal repayment.

- Interest payments are predetermined, regular payments back to investors. For private credit investors this can be different to traditional bank loans as they can leverage more flexible loan structures to reduce default rates.

- Principal repayment is where the borrower pays back the loan.

Returns for private assets, including infrastructure and real estate investments, can be impacted by a variety of reasons including but not limited to the global stock market and economic slowdowns, sector influences, regulation and the effects of energy conservation policies, competition, and the availability of fuel at reasonable prices.

Fees

There are two main types of fees typical in private markets’ investing: management fees and performance fees.

Management Fee

Investors are charged an annual management fee, typically around 1% to 2% of the capital they committed. This fee covers the costs of running the fund, including salaries, office expenses, and due diligence.

Performance Fee (Carried Interest)

Investors can also be charged a performance fee, often referred to as "carried interest." This fee is usually around 20% of the profits generated by the fund. It incentivises the fund manager to maximise returns for investors since they only receive carried interest after investors have received their initial capital back and a predetermined rate of return, usually referred to as the "hurdle rate."

Other Fees

Depending on the specific terms of the fund, there may be additional fees for services including but not limited to legal counsel, accounting, or transaction fees.

Private markets risks

As with any type of investing, private markets can offer financial rewards but they also come with their unique set of risks. Understanding these risks and your own tolerance for risk is essential for informed decision-making and a healthy investment approach.

Liquidity Risk

Unlike public markets where assets can be quickly bought or sold, private market investments often involve longer holding periods and can be harder to sell quickly. This could tie up your capital for extended periods.

Capital Risk

Investing in private markets often involves substantial upfront capital. If the investment doesn't pan out as expected, there's a risk of losing part or all of your initial investment.

Due Diligence Risk

Public companies are obligated to release business information publicly. Whereas private companies aren’t held to the same level of scrutiny or regulatory oversight. This makes thorough due diligence crucial to understand the business, its financial health, and growth potential – which requires professional knowledge and experience.

Market Risk

Private markets are not immune to the wider economic climate. Market downturns, changes in interest rates, and economic crises can affect the value and profitability of private investments.

Lack of Transparency

Private companies are not required to disclose as much information as public companies. This can make it more challenging for investors to assess the company's performance and potential risks.

Infrastructure

As a foundation of global economies, infrastructure represents a unique asset class with the potential to offer stability, inflation mitigation, and growth. This asset class could be pivotal in reshaping industries, supporting sustainable development, and driving economic growth worldwide. Explore how infrastructure investments hope to play a crucial role in advancing economic progress and fostering long-term value creation.

Infrastructure risk: Investment in securities and instruments of infrastructure companies can be affected by the general performance of the stock market and the infrastructure sector. In particular, adverse economic or regulatory occurrences including high interest costs in connection with capital construction programmes, high leverage, changes in and/or costs associated with environmental and other regulations, the effects of economic slowdown, surplus capacity, increased competition from other providers of services, uncertainties concerning the availability of fuel at reasonable prices, the effects of energy conservation policies and other factors can affect the value of infrastructure securities. Investing in infrastructure securities is not equivalent to investing directly in infrastructure and the performance of these securities may be more heavily dependent on the general performance of stock markets.

In a nutshell

Historically, governments shouldered the full burden of infrastructure financing like transportation hubs and water systems. This model, however, became challenging as public debt rose, leading to a pivotal shift towards private capital. Following the 2008 financial crisis, private investors—primarily institutional investors like pensions—stepped in to help bridge this funding gap3.

The financing gap

Responsibility for building and maintaining infrastructure has historically rested squarely with governments. Funded through public expenditure, this approach worked well under economic conditions that supported expansive budget allocations for critical public works. But the traditional model hit stumbling blocks in recent decades. It’s unlikely that today’s governments can pay for all the necessary infrastructure construction and maintenance on their own. That’s in large part because of the debt they carry, which has tripled since the mid-1970s, and now sits at 92% of global GDP4.

The situation across developed markets requires a strategic pivot toward private capital to bridge this funding gap. Private investors are meeting the need, led by institutional investors like large pensions.

These new investors have brought fresh capital to the table, stepping in to assume roles traditionally held by governments. They have acquired and managed municipal assets worldwide, with a mandate to try and optimise returns. This model aims to reduce the financing gap but also introduces a new dimension of efficiency and innovation in infrastructure management, leveraging private sector expertise.

Today, the transformation in infrastructure financing is evident. A broad spectrum of assets, from airports to railroads to water systems, now falls under this privatized management model, opening new investment avenues and highlighting the crucial role of capital in infrastructure development.

Investors now play a significant role in maintaining the infrastructure networks vital for economic growth and societal advancement. Often these investors can partner with government entities who can offer a reliable partnership, sharing some of the risks that accompany infrastructure projects. Public-private partnerships can take a variety of forms, such as private investors taking an equity stake in an airport or an operating agreement that could mean locking in long-term contracts, securing long-term cashflows. Low- and middle-income countries are frequent users of the public-private structure.

What is driving infrastructure investment today

Societies everywhere are grappling with major, overlapping challenges: energy security pressures, the transition to a low-carbon economy, changing demographics and urbanisation, and realigning supply chains. On the horizon is a digital revolution led by artificial intelligence. Taken together, these forces require an enormous amount of new infrastructure, from super batteries and hyperscale data centers to natural gas transport, from modern logistics hubs to airports.

Changing supply chains

Rapid technological progress in the past few decades has remade the world’s economies and societies. People are producing and using ever-increasing amounts of data and the trend is set to continue. The rise in remote work, video streaming and artificial intelligence has raised the demand for infrastructure projects. Digital proliferation at this scale needs infrastructure investment – to build, for example, the data centres essential for these new technologies.

Demographics

The global population is growing. By 2050, the global population will reach 9.7 billion people, up from 8 billion in 2022, according to the United Nations5. This growth will not be uniform across the globe. Developing nations need more infrastructure like transport systems, while developed nations can contend with smaller tax bases for upgrades and maintenance due to a shrinking working-age population.

There is no guarantee that any forecasts made will come to pass.

The digital future

Rapid technological progress in the past few decades has remade the world’s economies and societies. People are producing and using ever-increasing amounts of data and the trend is set to continue. The rise in remote work, video streaming and artificial intelligence has raised the demand for infrastructure projects. Digital proliferation at this scale needs infrastructure investment – to build, for example, the data centres essential for these new technologies.

The transition to a low-carbon economy

Government policies and incentives, widespread shifts in commercial priorities and practices, technology advances, and changing consumer and investor preferences are driving low-carbon energy investments. The transition will entail an overhaul of energy, transportation and related infrastructure – and that overhaul is already underway, with 2023 a record year for installations in both wind and solar power generation6.

Why do investors invest in infrastructure

A Natural Diversifier

Infrastructure assets offer unique diversification benefits due to their tangible, real-asset nature and typically lower correlation with public markets. This attribute provides potential downside protection, especially in periods of market volatility, helping to mitigate exposure to economic and real-rate risks.

Diversification and asset allocation may not fully protect you from market risk.

Inflation Mitigation

With inherent ties to inflation, infrastructure investments often feature revenue structures linked to inflation-adjusted contracts. Assets like power purchase agreements leverage pricing mechanisms to preserve purchasing power, while fixed maintenance costs further stabilize returns even in rising inflation environments.

Stable Cash Flow Potential

Infrastructure can help serve essential societal functions, driving consistent demand across market cycles. Long-term contracts and critical nature of these assets can potentially yield stable, predictable cash flows, aligning with investor goals for dependable returns over time.

Key infrastructure strategies

Income-Focused Strategies

Infrastructure debt, often structured to provide steady income for investors, finances essential projects through loans with variable terms and yields. Investment-grade debt typically offers stable, long-term cash flows, while high-yield and mezzanine debt—higher risk tiers—seek enhanced returns. Mezzanine debt, bridging debt and equity, entails greater risk but aims for strong yield.

Return-Focused Strategies

Equity-focused investments pursue growth in either brownfield assets—operational projects offering steady income with lower risk—or greenfield assets, pre-operational developments with high capital growth potential but greater risk including construction delays.

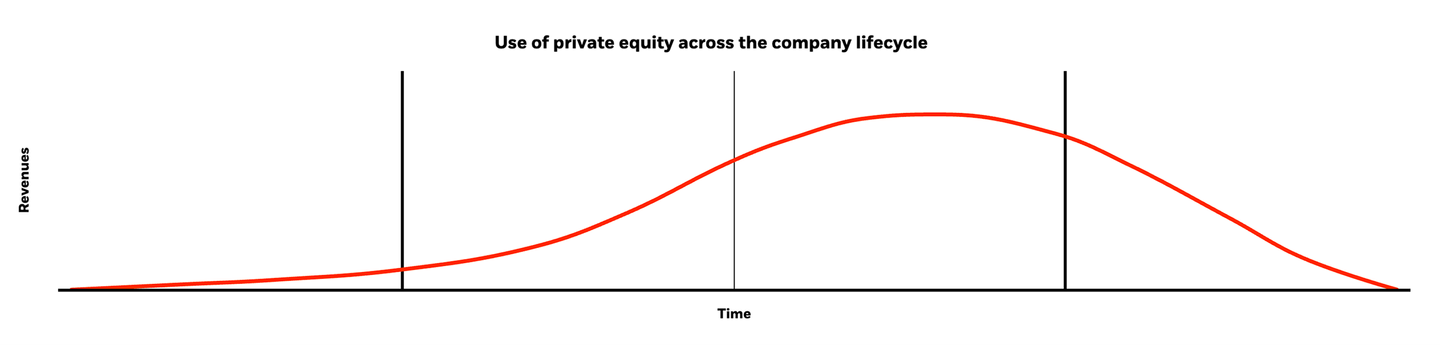

Private equity

Private equity (PE) involves investing in privately held companies, from early-stage startups to established firms, with the aim of growing their value and eventually selling them for a profit.

In a nutshell

Private equity (PE) is the most common form of accessing private markets and was born out of the industrial revolution near a century ago. It involves investing capital into privately held companies that are not available on public stock exchanges, in return for a stake in the company or ownership.

Buy

Private equity managers, or general partners (GPs) raise capital from various investors and pool funds together into a private equity fund. This then gets invested into individual private companies, from early-stage startups to established companies.

Improve

GPs manage the fund and aim to help these companies grow and become more profitable, leveraging various value creation strategies like reducing operational costs, paying off debt, or implementing a growth strategy. This can take many years, so individual investors need to be prepared to invest for the long-term.

Sell

If the company becomes more valuable, GPs will look to sell and exit the investment for profit. This could be through selling to another company or through an initial public offering (IPO), selling shares to the public.

Risk: GPs may not be successful in growing or making companies more profitable.

PE is big and more accessible than ever

The private equity market is huge, as most companies are privately held7. Public markets are now only a fraction of the size of the total equity market and are shrinking, while private markets are growing fast8.

For years institutional investors have been investing in private markets to grow their portfolios and governments have introduced regulations to make private markets more accessible to individual investors9.

Unlocking value in private companies

Not only are there more private companies, but they are also staying private for longer10. This longer holding period allows GPs to implement strategic initiatives and drive corporate change, potentially maximising value creation and delivering potential higher returns for individual investors.

This potential success can be attributed to PE managers' focus on long-term value creation through active and entrepreneurial approaches.

Examples of value creation

Strategy Development

Defining and developing a long-term strategy to guide the company's growth and operations.

Internationalisation

Expanding the business geographically to tap into new markets and increase revenue.

Cost Optimisation

Implementing operational improvements to reduce costs and increase efficiency.

Capital Measures

Paying down debt and reducing the financial burden to improve the company's financial health.

Growth

Focusing on developing successful business areas and making strategic acquisitions to drive expansion.

Potential rewards and risks

Private equity may come with potential greater financial reward, but it also comes with greater risk. Investing in private companies poses different risks compared to listed companies, with illiquidity being a key concern. Illiquid investments are hard to convert into cash without significant loss in value, making it difficult to withdraw money as funds are typically locked up for the investment term. However, investors could expect higher returns in exchange for holding illiquid assets, known as the illiquidity premium.

Key private equity strategies

There are different stages of private equity funding and how it can help companies create value and grow. Typically, GPs look for companies that offer growth potential or that, in their view, are undervalued with room to improve. They usually aim to invest over a period of several years.

Venture Capital

Investing to fund a new idea and/or early stage company.

Stage: Early to mid

Risk & return11: Very high

Typical investor: Minority

Exit strategy: IPO12 or sale

Cash flow: Negative

Growth

Capital injection designed to strategically change or improve a company.

Stage: Late

Risk & return11: Moderate

Typical investor: Minority

Exit strategy: IPO or sale

Cash flow: Break-even/positive

Buyout

Takeover of a company, typically by using borrowed funds (leveraged buyout), targeting company/divisions that have been neglected in terms of capital investment/ management etc.

Stage: Mature

Risk & return11: Moderate

Typical investor: Majority/control

Exit strategy: IPO or sale

Cash flow: Positive

Special situations

Investing in established companies that face operating, financial or other challenges.

Stage: Mature or underperforming

Risk & return11: Moderate to high

Typical investor: Situationally dependent

Exit strategy: Restructuring or sale

Cash flow: Positive

Important information. For illustrative purposes only and subject to change.

Ways of accessing private equity funds

To invest in private equity there are key transaction types to be aware of. We have primary, secondary and co-investment transactions.

Short of making a direct investment into a company, the most straightforward route is a primary transaction. A GP creates and manages a PE fund and finds limited partners (LPs) who are minority investors, to invest alongside them in this PE fund, which then invests into individual companies.

Then we have a secondary transaction where we see investors buying into the fund by taking on the fund commitments of existing LPs, who wish to make an early exit.

Then third transaction type are co-investments, which allow other investors to put capital directly into selected companies alongside the PE fund as a minority owner. Co-investors have the same rights as LPs. GPs offer co-investments to raise additional capital as well as avoiding concentrating too much capital into a single portfolio company.

Fund structures and how it impacts fees

Whether a fund has a closed-ended or open-ended fund structure has a bearing on how management and performance fees are charged.

Most private markets’ investments are closed-ended, which typically means they have a fixed number of shares, are less liquid, and investors buy and sell those shares at market price.

Fund structure

- Closed-ended funds have a specific fund term, typically 8-10 years. GPs have a limited window to raise capital, and once this window expires no further investments can be raised – known as a limited investment period. Typically, investors cannot redeem any of their investment before the fund sells.

- On the other hand, open-ended funds have extended fund terms, e.g. 99 years. These types of funds issue new shares based on investor demand, have some form of liquidity, and investors can trade more easily. As a result, these types of funds make investments on an ongoing basis. They are also known as evergreen funds.

Fees

There are two main types of fees in private markets’ funds: management and performance fees.

- Management fees cover the cost of managing the fund, including due diligence, monitoring and administrative expenses.

- Then there is a performance fee, generally a percentage of the profits earned by the fund and is paid to the fund manager if certain performance targets are met. It can incentivise the fund manager to maximise returns for investors.

Closed-ended funds pay an annual management fee, typically 1-2% of the capital committed, and a performance fee usually of around 20%.

However, the fees are charged differently for open-ended funds. It depends on the fund’s real value at a specific point in time, also known as the fund’s Net Asset Value (NAV): total assets minus total liabilities. Both management and performance fees are charged based on the fund’s NAV, while the performance fee is still subject to a certain performance target being met.

The mechanics behind distributions

Over the lifespan of a PE fund, individual investors may start to receive dividends or distributions as the companies within the fund mature or are sold. The order in which returns are distributed to the involved parties is known as the "waterfall".

The Waterfall of Returns

1

Return of Capital

100% to Investors: All distributions go to investors until they have received back their initial investment.

2

Preferred Return

100% to Investors: All distributions go to investors until the fund has reached the percentage of profits set as a benchmark, known as the preferred return. This can also be referred to as the ‘hurdle rate’, which is the minimum return before GPs can earn any performance fee.

3

Carried Interest for GP

The GP Catch-Up: Once the hurdle rate is reached, the GPs earn a performance fee (or carried interest) on the profits earned to date, effectively "catching up".

4

Remaining Distributions

Split Between Investors and GP: Depending on the fund's terms, the remaining distributions are split between the investors and the GPs.

Private credit

Private credit represents part of the broader alternative’s universe, referring to non-traditional assets that provide flexible lending solutions. Private credit generally offers higher returns compared to public corporate bonds and loans. This is because investors are compensated for investing in less liquid markets, known as the illiquidity premium.

In a nutshell

Private credit, also known as private debt, refers to lending conducted outside traditional bank lending channels or public debt markets. Unlike traditional lending markets where banks arrange and syndicate loans to large groups of lenders, private loans are typically originated directly between a corporate borrower and a small group or a single lender. These loans are negotiated directly by companies that do not have, or have limited, access to public corporate bond and loan markets. Most of these companies are medium-sized and referred to as "middle market" companies.

Private credit covers a broad spectrum of lending strategies, including opportunistic and distressed debt, and middle market or direct lending.

The asset class became more prevalent when banks reduced lending following the Global Financial Crisis of 2008-9. The introduction of new regulations (Basel III) required banks to hold more capital against loans, making it less capital-efficient to lend to certain businesses. Consequently, private lenders have increasingly stepped in to fill the gap due to their ability to move quickly and provide bespoke, customised loans that can better meet some businesses’ needs.

Reasons companies seek private credit

The reduction in bank lending and the increasing deal sizes in syndicated markets are driving borrowers to seek financing from alternative sources. Borrowers choose private debt for several reasons:

Certainty of execution

Borrowers prefer the simpler and less resource-intensive processes in private markets compared to public markets.

Flexibility

Private debt solutions offer more flexibility in loan terms and structuring than traditional financing.

Long-term partnership

Private lenders can have a deep understanding of a borrower's business and financing needs over time, allowing them to provide financing packages that enable companies to achieve their growth potential.

The advantage of a non-bank private loan is that there is typically more flexibility. The business can grow without equity being given away and private lenders can often act more quickly.

Benefits for investors

Private credit offers a range of potential benefits:

Diversification

Private debt can help to diversify investment portfolios with potential returns that don't closely follow public stocks and bonds. Diversification means spreading your investments across different asset classes, sectors, or geographic regions to reduce the impact of any single investment's poor performance on your overall portfolio. This low correlation with public markets may allow private debt to help spread out risk and potentially improve overall returns.

Diversification and asset allocation may not fully protect you from market risk.

Inflation mitigation

Private credit loans are primarily structured as floating rate which provides some protection against rising interest rates – as interest rates increase the interest the business pays on loans increases accordingly. The interest could provide a reliable income stream that is less susceptible to market fluctuations.

Downside mitigation

Compared to traditional lending, private lenders have greater say over terms and pricing and are better able to negotiate covenants designed to protect investor’s interests. Private lenders could secure investor protections by having an open dialogue with the borrower to better understand and anticipate periods of stress.

Return premiums

Private debt can provide steady income and is usually less affected by market volatility due to its lower correlation with public market fluctuations. Historically, it has offered the potential for reliable income through extra returns from less liquid investments (illiquid premium) and has often done better than traditional bank loans and bonds over the long term. However, it's important to note that private market investments can also face challenges, such as reduced liquidity during stressed market conditions.

Key private credit strategies

The private credit market has evolved significantly since the Global Financial Crisis (GFC), offering a wide range of strategies to meet investors' return objectives with varying risk and return profiles. These strategies can generate cash flow and often have shorter durations compared to other private investment strategies. Investors can build portfolios to provide income, benefit from when markets are under stress, and diversify away from concentrating investments into individual companies.

Each category of private credit serves a distinct purpose and borrower profile, with its own terms and conditions (e.g., interest rate, maturity, seniority (who gets paid first if a company goes bankrupt), security, covenants), leading to unique risk and return characteristics. Some of the most relevant credit strategies include:

Direct lending

Direct lending is a form of private debt where the lender provides financing directly to the borrower, typically a small to midsize enterprise (SME) or middle-market company, without involving traditional banks. The debt is usually senior and secured, with a range of covenants in place to protect the lender or investors.

Opportunistic credit

Opportunistic credit refers to a strategy within private credit that focuses on providing capital solutions to companies throughout different stages of credit access known as the credit cycle. This strategy is designed to take advantage of market dislocations, distressed situations, and other special opportunities that arise due to changing market conditions. Opportunistic credit investments often involve higher risk but can offer higher returns compared to more traditional credit investments.

Special situations

Special Situations refer to investment opportunities that arise from unique circumstances affecting a company, such as financial distress, restructuring, or other significant events.

Important information. For illustrative purposes only and subject to change.

BlackRock

As a global investment manager and fiduciary to our clients, our purpose at BlackRock is to help everyone experience financial well-being. Since 1999, we've been a leading provider of financial technology, and our clients turn to us for the solutions they need when planning for their most important goals.

© 2026 BlackRock, Inc. All Rights Reserved.