Helping build a pathway towards retirement spending and

income confidence

Something unexpected has been the shared experience for many of our most recent generation of retirees that will reverberate across the investment and insurance industries. The vast majority haven’t been spending their retirement savings—leaving nest eggs mostly untouched and living on ready sources of income instead. However, future retirees may be less fortunate, and may need to spend down principal in order to fund their spending needs. In this paper, we summarize the findings of The BlackRock Retirement Institute’s research and white paper, Spending retirement assets…or not?1 and provide a framework for advisors to engage with their clients around the challenges in store as they transition from asset accumulation to retirement income.

Key findings:

- On average across all wealth levels, most current retirees still have 80% of their pre-retirement savings after almost two decades in retirement

- More than one third of current retirees actually grew their assets—leaving considerable potential consumption on the table

- The financial landscape for future retirees will most likely be more challenging, requiring different savings and spending behaviors

- Future retirees are going to need retirement income solutions that can provide spending confidence—for both essential spending needs and more discretionary “wants”—and insurance solutions can play an important role within an integrated retirement income and investment strategy

- The potential role of insurance can be better understood with the use of illustrative tools that show investors how well insurance products can be integrated into investment plans to fully optimize hard-earned savings in retirement and spend with greater certainty

The soaring number of Baby Boomers entering and approaching retirement is leading to a major shift in focus from accumulation and retirement savings to decumulation and retirement income. This demographic “tipping point” already occurred in 2013/2014 with assets leaving 401(k) plans exceeding assets being contributed or entering plans.2 This trend is expected to remain until 2030, peaking at $40 billion annually in 2019.3

Most people approaching retirement today are uncertain how they will manage their retirement assets with an eye towards decumulation—the conversion of assets into income. Indeed, we’ve heard from many advisors how important it is— and how challenging it can be—to get clients to understand the relationship between assets, income and retirement goals. Many don’t realize what advisors know all too well: living longer in a historically low interest rate environment may lead to a gap between what their current savings can generate and the retirement income they are expecting.

Retiree spending behaviors

In order to better understand how people will cope with the transition to decumulation, the BlackRock Retirement Institute (BRI) in conjunction with the Employee Benefit Research Institute (EBRI) looked backward to observe the actual spending behavior of retirees who have been living in retirement over the last two decades. What the study found was quite interesting: instead of actively and systematically decumulating assets, retirees displayed a tendency across all wealth levels to retain assets and not spend down their initial principal. However, future retirees may be less fortunate.

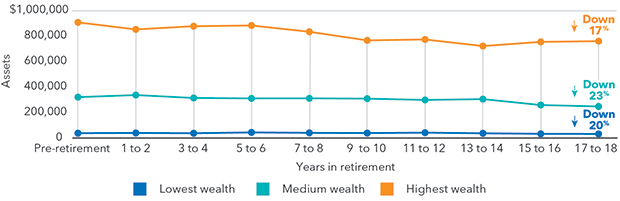

The study segmented retirees into three groups based on pre-retirement non-housing assets4—$0 to less than $200,000 (lowest wealth), $200,000 to less than $500,000 (medium wealth) and $500,000 and above (highest wealth). The drop in median, non-housing assets right before retirement compared to a maximum of 17-to-18 years into retirement remains remarkably steady across the time period with the highest wealth group retaining the most assets (83%), followed by the medium and lower wealth groups at 77% and 80%, respectively (Figure One).

Figure one: Median non-household assets

Source: Employee Benefit Research Institute estimates based on Health & Retirement Study (HRS, 1992-2014). Consumption and Activities Mail Survey (CAMS, 2005-2015)

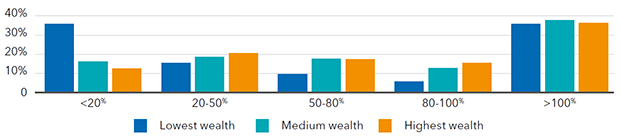

Figure two: Percentage of assets remaining after 17-to-18 years of retirement5

Source: Employee Benefit Research Institute estimates based on Health & Retirement Study (HRS, 1992-2014). The HRS Survey used a sample of 7,148 retiree households who provided self-reported asset data.

However, medians don’t mean everyone is not spending down, or adding assets, and Figure Two provides a fuller picture behind the averages. We separated our three asset level groups further in terms of percentage of assets remaining after 17-to-18 years in retirement—those with less than 20%, 20 to 50%, 50 to 80%, 80 to 100% and more than 100%. Across the three wealth groups we do see some spend down of assets especially with the lowest wealth group. But we also see remaining assets increasing for over 35% of all participants. This supports prior research6 that suggests households tend to preserve retirement assets, with rates of returns on those assets often exceeding withdrawals, resulting in asset balances for many retirees growing through at least 85 years old.

Most retirees are spending in line

with income

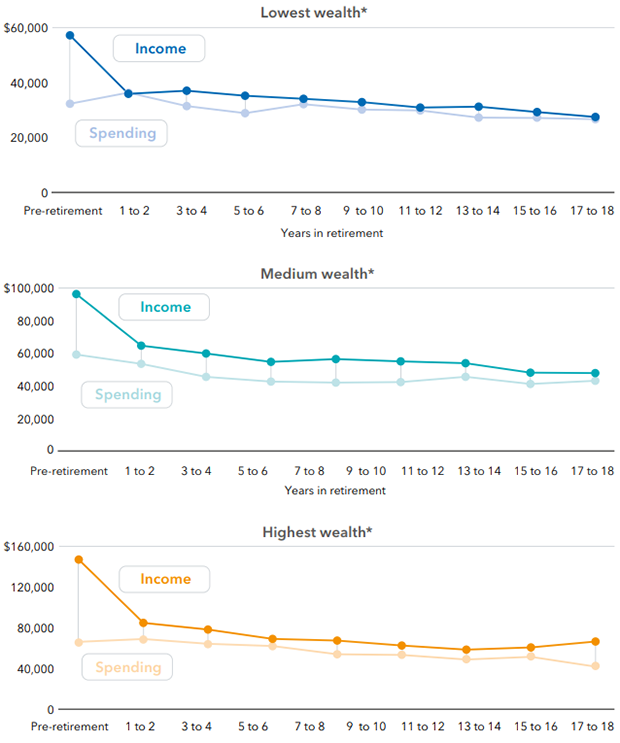

If most retirees aren’t aggressively drawing down assets, then what have been their other main income sources? Outside of retirement savings principal, we observed that income in retirement is generally derived from four sources: labor, capital7, pensions, and Social Security, with social security contributing the largest portion to all three wealth groups. After an expected drop from pre-retirement, income levels remain fairly steady with a slight decrease over time—with after-tax replacement ratios basically in line with the 60 to 70% rule of thumb, depending on preretirement income levels. Spending levels hover right below income with the wealthiest group showing the largest spending drop over time (Figure Three).

One relief valve for the highest wealth group and to a lesser degree the medium group could have been capital appreciation from their investment portfolio. During the 1992-2015 period a conservative hypothetical 20% equity—80% fixed income portfolio and a more aggressive hypothetical 60% equity—40% fixed income portfolio delivered annualized returns of 6.6 and 8.0%, respectively.8 Accessing these appreciated assets would likely contribute to any shortfall without reducing principal. So it would seem that most retirees are able to retain a reasonable standard of living by simply adjusting spending levels based on income, leaving savings principal barely touched.

Figure three: Median annual pre-tax income and spending9

* Measured in 2015 dollars.

Looking back: most didn’t need to or didn’t want to spend savings

Over almost two decades, retirees in our study mostly refrained from spending down assets and lived off of other sources of income instead. We believe many could have afforded to withdraw a little and, in some cases, a lot more from their retirement accounts but chose not to, potentially leaving large amounts of hard-earned savings unspent. There may also be a more deep-seated behavioral biases, including the lack of confidence and hesitation to spend their nest eggs after being told for years to “save, save, save.” A BlackRock survey found that only 36% of Americans are confident they will have the income they need in retirement—while 55% are concerned about outliving their savings in retirement.10 Without thoughtful, trusted guidance, such fears and lack of planning could have dire consequences for the next generation seeking income to hopefully sustain a consistent standard of living.

Looking forward:

A more challenging environment

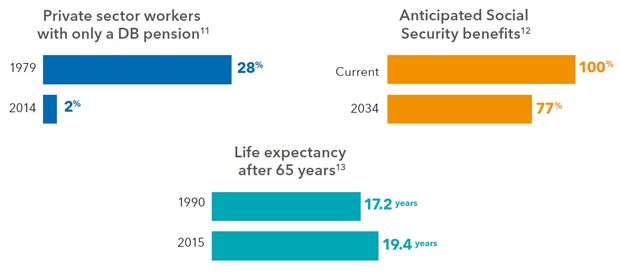

Those retiring in the 1990s and 2000s had many tailwinds lessening the need and desire to systematically tap into savings principal in order to maintain a reasonable standard of living in retirement. Looking ahead, future retirees may not be so lucky. They will likely retire into an environment with multiple headwinds and face growing pressure to save more and maximize the value of their entire retirement savings— principal and all—unless they are willing/able to make dramatic cuts in their retirement lifestyle. We see several major challenges over the horizon—from lower investment forecasts, a lack of defined benefit (DB) pension income, lower expected Social Security benefits to longer life expectancy (Figure Four). These structural and societal uncertainties along with the more subtle behavioral roadblocks already inherent in retirement spending suggest a challenging environment in the coming decades.

Figure four: Mounting obstacles to retirement success

Decumulation in retirement: The second act

For these future retirees—living longer with very few drawing guaranteed retirement income beyond social security—the need to generate reliable lifetime income will be much greater. But systematically drawing down assets is complex. According to Transamerica, 47% of American workers say they have simply “guessed” as to their retirement savings needs—14 more than double the next highest response—leaving them open to potentially spending down assets at an unsustainable rate or underspending out of fear of outliving their money. That’s why it’s important for investors to begin to focus on their future retirement income goals and spending needs before retiring and start thinking through ways they can maximize the income producing potential of their hard-earned retirement savings alongside their expected Social Security benefits.

Optimizing retirement income solutions

Research from the Stanford Center on Longevity15 looked at ways investors can potentially assess and combine a mixture of investments and insurance products against different retirement income goals. They evaluated systematic withdrawal plans (SWPs) for investment portfolios and basic annuities against the following criteria:

- Amount of income

- Access of savings

- Pre- and post-retirement protection

- Inflation protection

- Lifetime guarantee

One of the key findings from their research was that from a purely financial perspective, annuities often provide higher yearly income as compared to systematically withdrawing from investment assets. However, from a behavioral perspective—in particular access to savings—100% annuities or even a substantially high degree of annuitization would be suboptimal for most people. The report suggests a more balanced approach might be to first apply a portion of retirement assets to purchase an annuity that provides guaranteed income16 that, along with Social Security, could cover essential spending needs. A SWP17 could be applied to the remainder of retirement savings to cover discretionary expenses. Their report also stressed the importance of protecting assets from market declines during the critical period five to ten years preceding retirement, encouraging investors to reduce equity risk in their portfolios and consider purchasing deferred annuities.

The research by Stanford and others reinforces the complexity and risks when tackling retirement income, leaving a heightened need for investor guidance. To help close the knowledge gap between where investors are today and the annual income they want to maintain their standard of living in retirement, BlackRock has developed a technology platform for both the accumulation and decumulation phases that seeks to build greater clarity around lifetime income.

iRetire®: A new framework for 21st century retirements

BlackRock’s iRetire is a retirement technology platform that provides value to both advisors and their clients through a dynamic and robust retirement planning process that spans the entire lifecycle of retirement planning. To do this, the iRetire platform brings together some of BlackRock’s best technology, investment and partner firm insurance expertise and advisor support to provide an effective, interactive and scalable process for saving, investing and spending decisions over time. This process is driven by BlackRock’s exclusive CoRI® methodology, which translates savings into income by tracking daily the estimated cost of annual lifetime retirement income.

Figure five: How iRetire works

| Pre-retirement iRetire helps investors: | In retirement iRetire helps investors: |

|---|---|

| Understand the relationship between assets and income | Consolidate and manage trade-offs from income sources |

| Aggregate all sources of potential income | Estimate a sustainable spending rate and adjust as needed |

| Close potential gaps to desired income goals | Illustrate the impact of adding annuitybased income leaving the flexibility to purchase additional annuities at any point |

Make clearer decisions based on personal preferences:

|

Make clearer decisions based on personal preferences:

|

| Journey manage to stay on track with as needed course corrections | Journey manage to stay on track with as needed course corrections |

When working with clients who are still saving for retirement, advisors can use the iRetire platform to help them to better understand how current and future savings behaviors and assets translate into estimated lifetime income in retirement. iRetire platform capabilities also include the ability to allocate a portion of savings to a partner firm's annuity product that provides guaranteed income,18 so the advisor can use iRetire to help clients understand preferences for risk vs. secure income and help make informed decisions on how much annuity allocation is appropriate, based on the clients’ goals.

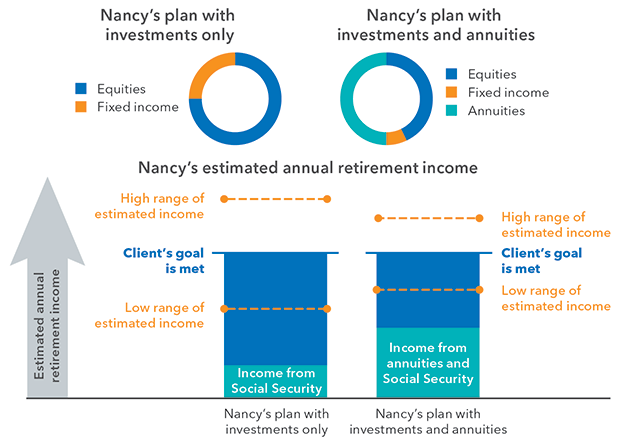

Case Study: Pre-Retirement

Nancy is a 55 year-old investor, ten years away from retirement. Working with her advisor, the iRetire tool indicates that attaining her income goal beyond the amount she anticipates receiving from Social Security with investments alone could require a very aggressive investment approach in her last ten years of working and accumulation (leaving her vulnerable in the event of a market downturn). Nancy’s advisor runs her iRetire simulation with a 50% allocation to a deferred lifetime annuity and finds that this adjustment could provide enough guaranteed income at retirement to allow for a significantly reduced risk level for her remaining investment assets over her last ten working years—while still being on target to achieve her overall retirement income goal.

Figure six: Using iRetire can help narrow estimated income ranges

For illustrative purposes only and not representative an actual account. Actual outcomes will vary. Product selections vary per iRetire platform. BlackRock does not offer insurance products or provide any financial guarantee of periodic payment. Annuities are issued by one or more insurance companies.

Conclusion

Journey management: build confidence and support outcomes

When working with clients who are still saving for retirement, advisors can use the iRetire platform to help them establish a baseline to better understand how current and future savings behaviors and assets translate into estimated lifetime income. For clients who are retired, advisors can use the iRetire platform to track progress by estimating the sustainable annual income they could generate at each stage of retirement and mapping out a flexible plan around short-term spending, investment portfolio selection and new and additional insurance products, such as a single premium immediate annuity (SPIA). The iRetire platform can then be an effective re-engagement tool for advisors to help clients stay on track and be positioned for the income they want to support their desired spending over the course of their retirement.

Shifting demographics and a more challenging financial market environment will only elevate the complexity and importance of helping retirees maximize the value of retirement savings to attain a certain standard of living. Future retirees will face financial and longevity risks not seen by prior generations as well as many of the apparent behavioral spending biases holding back current retirees from fully enjoying their hard-earned retirement savings. Whether they can gain the confidence to spend retirement assets when and if needed—or not and potentially see major adjustments to their lifestyle instead—remains to be seen.

At BlackRock we have studied these retirement challenges extensively and have concluded that the tools needed to address retirement income readiness exist—but not in a single solution. In order to engender more widespread adoption, solutions should be integrated and presented to retirees in ways that are easy to understand and implement. Thanks to rapid advancements in financial planning technologies such as iRetire, coupled with innovative financial solutions currently available, we are confident that a combination of insurance, investments and planning/ education technology can go a long way towards helping retirees attain greater income certainty and spending confidence as they embark on 21st century retirements.

Appendix

Inside BlackRock’s CoRI Indexes The iRetire® calculations use daily data from BlackRock’s exclusive CoRI methodology, which tracks the estimated cost of annual lifetime retirement income. In pre-retirement, as investors are getting to retirement, the CoRI values help determine the gap between current estimated retirement income and their desired retirement income goal. In retirement, as investors are getting through retirement, the CoRI values help determine a sustainable annual income estimate that investors can withdraw each year while maintaining enough savings to purchase a comparable income stream from a guaranteed source, such as an annuity, at any point if desired.

Income estimates based on CoRI methodology automatically account for longevity because the methodology incorporates four key factors that affect the cost of retirement income:

Age until 65: As your client gets closer to age 65, there’s less time for interest rates and market returns to mitigate the cost of retirement.

Interest rates: The wild card in the retirement calculation, changes in interest rates can significantly impact the price of income.

Inflation: Preserving purchasing power by incorporating a cost of living adjustment (COLA) increases the cost of retirement income.

Life expectancy: After she turns 65, your client can expect fewer annual retirement income payments, reducing the cost of funding her remaining retirement.