The Ministry of Finance appointed the 10th governor of the Bank of Canada last week amid an unprecedented economic slowdown, pickup in fiscal deficits and central bank purchases of government bonds. Kurt and Daniel explore what large-scale asset purchases at a time of ever higher deficit projections could mean for financial markets.

This past week brought many new developments related to the future of Canadian monetary policy and its relationship with fiscal policy in the post-coronavirus era. First, Finance Minister Bill Morneau announced on Friday that Tiff Macklem would begin his seven-year term as the next Governor of the Bank of Canada (BoC) after current Governor Stephen Poloz steps down on June 1. Macklem, currently the Dean of the Rotman School of Management at the University of Toronto, was previously senior deputy governor of the Bank of Canada under Governor Mark Carney and recently chaired the government’s Expert Panel on Sustainable Finance, which published its final report in 2019.

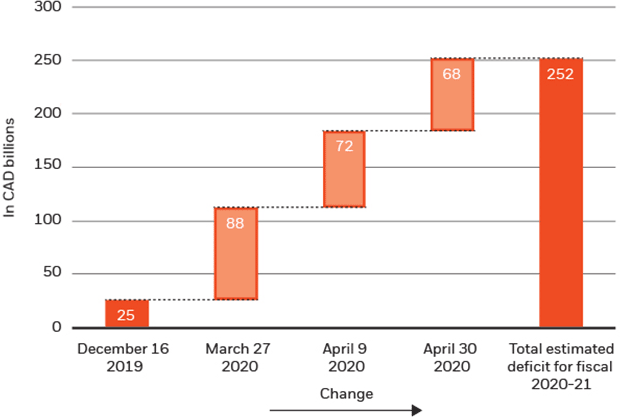

Second, the Parliamentary Budget Officer (PBO) updated its Covid-19 scenario analysis last week and now projects the federal budget deficit to rise to C$252 billion (12.7% of GDP) for the 2020-21 fiscal period. As a share of the economy, the 2020-21 budgetary deficit is expected to be the largest on record. The PBO’s macroeconomic scenario assumes a 12% decline in Canadian GDP in 2020, and a US$16/barrel average price for West Canada Select oil prices in 2020, well below profitable levels for Canadian energy companies. The 2020-21 budget deficit worsens in two parts from the prior C$184 billion estimate in early April: C$27 billion from automatic stabilizers and a worsening economy and C$40.5 billion additional spending for a total of C$146 billion in Covid-19 relief (see the chart below). This brings Canada’s fiscal spending to 7.3% of estimated 2020 GDP.

Change in federal government deficit estimate, fiscal 2020-21

Source: BlackRock Investment Institute, with data from the Office of the Parliamentary Budget Officer (PB0) and the Department of Finance Canada, as of 30 April 2020.

Notes: The original 2020-21 budgetary deficit forecast of $25B is from the December 2019 Economic and Fiscal update. The March 27, April 9, and April 30 updates are based on the Scenario Analysis reports published by the PB0.

Without central bank purchases and near-zero policy rates, the growing federal indebtedness would almost certainly imply higher interest rates. The next governor of the Bank of Canada will have to carefully modulate its bond purchases to ensure that financial conditions remain consistent with the central bank’s goal of ensuring price stability. Already since March when the BoC announced special policy measures in reaction to the coronavirus to improve market functioning and liquidity, total assets on the BoC’s balance sheet have grown from C$120 billion to over C$380 billion, principally owing to its buying of treasury bills, Government of Canada securities and conducting overnight and term repo operations (see the chart below).

Weekly net purchases by the Bank of Canada, 2020

Source: BlackRock Investment Institute, with data from the Bank of Canada, as of 29 April 2020.

Notes: The chart shows the weekly change in assets held by the Bank of Canada. Securities purchased for resale includes the bank’s Overnight Repo and Term Repo Operations- Examples of “other" assets includes provincial money market securities, Canada Mortgage Bonds, bankers’ acceptances, and commercial paper.

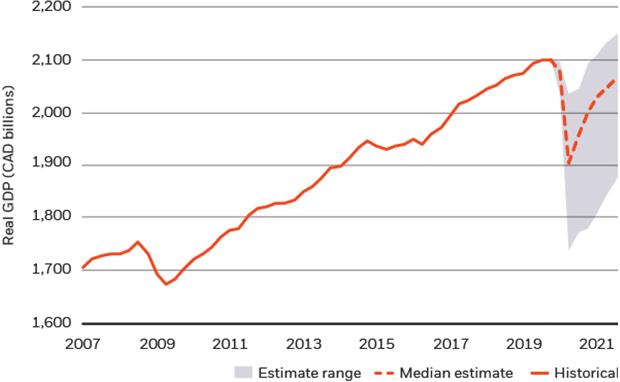

We assume the BoC will finance the growing federal deficits by purchasing much of the new Government of Canada bond issuance to limit the backup in interest rates and an unwanted tightening of financial conditions. At the current pace of C$7-8 billion per week, this would mean the BoC would own Government of Canada bonds equivalent to 15-17% of GDP by March 2021. Assuming a steep decline in economic output to begin 2020 as well as a slow recovery for the energy sector and household consumption over subsequent quarters (see the chart below), deficits may have further to rise. But even if they did, this would likely imply even greater BoC bond purchases than the current trend.

Hypothetical hit to Canadian GDP, 2020

Source: BIackRock Investment Institute with data from Bloomberg, Refinitiv Datastream, and Statistics Canada, as of 1 May 2020.

Notes: The chart shows hypothetical pathways of Canada’s real GDP (2012 chained dollars) based on a survey of 16 economist estimates from Bloomberg. The estimates are dated from 13 April to 1 May. There is no guarantee that any forecasts made will come to pass.These hypothetical scenarios are subject to significant limitations given the uncertainties surrounding the virus outbreak-

In our view, central banks will likely be keen to limit interest rate increases after the coronavirus crisis passes while at the same time supporting a firming of inflation expectations. Amid sustained low nominal interest rates, these efforts would likely weigh on the real return of government bonds and raise questions about their strategic portfolio diversification benefits. For more on our strategic case for reduced long-term holdings of nominal government bonds, please see our global weekly commentary.

Kurt Reiman

Stratège principal pour l’Amérique du Nord, BlackRock

Kurt Reiman, directeur général, est membre du BlackRock Investment Institute (BII) et est stratège principal pour l’Amérique du Nord. Dans le cadre de ses fonctions, ...