RETIREMENT CENTER

Investing in a better retirement starts here

Retirement is more complex than ever. We’re helping make it more accessible by providing answers and insights, no matter where you are on your journey.

Retirement 101

Take a full class on retirement by exploring our complete educational library. Here you can study different topics to help find the answers you’re looking for.

Get the latest Read on Retirement

Two years of rising inflation, volatility and a global pandemic reveal that savers are looking for greater security in this year’s annual retirement survey.

Educational videos

Learn about retirement and how to help prepare with short videos that explain key investing concepts.

-

![]()

Thinking about retirement from the start

-

![]()

Staying on track with your goals

-

![]()

Getting ready for retirement

-

![]()

Pay your future self first

-

![]()

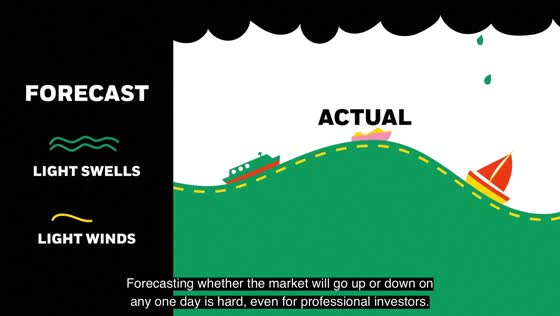

Understanding market volatility

-

![]()

Learn how target date funds work

-

![]()

Simplify retirement investing

-

![]()

Diversification and target date funds

Retire from work, not a paycheck

A new generation is entering retirement dependent almost entirely on savings and will need help generating sustainable income. BlackRock is working with insurers and leveraging technology to reimagine retirement for millions of American workers.